Macias Gini & O’Connell’s articles from MGO CPA LLP are most popular:

with readers working within the Basic Industries, Business & Consumer Services and Construction & Engineering industries

MGO CPA LLP are most popular:

within Real Estate and Construction, Law Practice Management and Law Department Performance topic(s)

Key Takeaways:

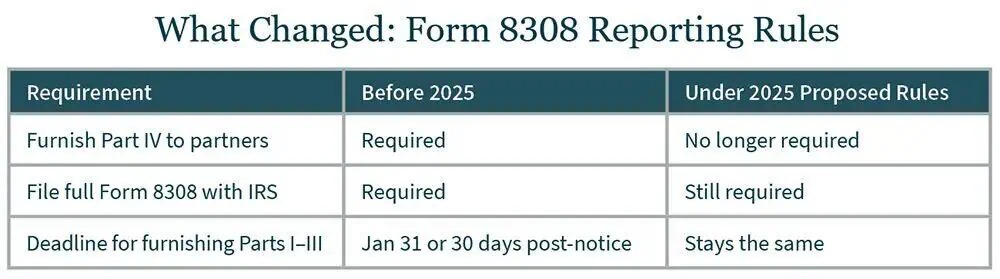

The IRS has proposed rules eliminating the need to furnish Part

IV of Form 8308 to partners in most cases.

Partnerships must still complete full Form 8308 and file it

with Form 1065, but new relief simplifies what is sent to

partners.

These changes apply to Section 751 exchanges occurring in the

2025 tax year, and offer welcome certainty after two years of

temporary relief.

Partnerships dealing with Section 751(a) exchanges — those

involving so-called “hot assets” like unrealized

receivables or inventory items — have faced mounting reporting complexity over the past

several years. Form 8308, which must be furnished to

transferor and transferee partners in these exchanges, was

significantly expanded in late 2023. But in 2025, the IRS proposed

regulations offering targeted relief that streamlines these

reporting obligations.

Private companies operating through

partnerships should understand what has changed, what is still

needed, and how to remain compliant.

The Burden of Expanded Form 8308 Reporting

The revised Form 8308, released in October 2023, introduced new

Parts III and IV, significantly increasing the reporting burden for

partnerships involved in Section 751(a) exchanges. These exchanges

occur when a partner transfers their interest, and some of the

proceeds relate to unrealized receivables or inventory —

assets that trigger ordinary income treatment rather than capital

gain.

Under earlier rules, partnerships were expected to furnish the

full form — including detailed breakdowns of ordinary income,

collectible gains, and unrecaptured Section 1250 gain — by

January 31 following the year of the transfer. In many cases,

partnerships lacked the data needed to complete Part IV by that

deadline, especially when notice of the transaction came late or

data from transferor partners was incomplete.

Recognizing the compliance challenges, the IRS offered temporary

relief through Notice 2024-19 and Notice 2025-02. But that relief was short-term,

and uncertainty stayed.

What the Proposed Regulations Change

In August 2025, the IRS issued proposed regulations that address

the most problematic aspect of the expanded Form 8308: the deadline

for furnishing Part IV to transferors and transferees.

Under the proposal:

Partnerships no longer need to offer Part IV to partners by

January 31 (or within 30 days of receiving transaction

notice).

They still must give Parts I, II, and III to the transferor and

transferee within the standard timeline.

Part IV must still be completed and attached to the partnership

Form 1065 for the tax year that includes the exchange.

This distinction is important: the IRS still wants complete

information, but the burden of giving it directly to partners under

tight deadlines has been lifted — at least for now.

When the Changes Apply

The proposed rules apply to Section 751(a) exchanges occurring

on or after January 1, 2025, and are effective

immediately — even though final regulations have not yet been

issued. This gives partnerships more certainty as they close their

books for 2025.

The IRS also plans to revise the instructions to Form 8308 to

align with these rules.

What Hasn’t Changed

While the furnishing burden has been eased, other obligations

are still intact:

Partnerships must still decide if a Section 751(a) exchange

occurred.

The full Form 8308, including Part IV, must still be filed with

the IRS and attached to the partnership Form 1065.

Statements must still be furnished to both transferor and

transferee with accurate and timely information for Parts

I–III.

Penalties under Section 6722 may still apply if needed

information is incomplete, inaccurate, or delivered late.

For exchanges where the partnership receives delayed notice

— or where details of unrealized receivables or inventory are

not available — these clarifications offer some

administrative breathing room.

Practical Planning Considerations

As partnerships consider year-end tax filings and upcoming

transactions, several steps can help reduce risk and improve

compliance:

Evaluate your current 8308 process: Confirm whether you are

prepared to distinguish which parts must be furnished versus

filed.

Communicate early with transferor partners to gather any needed

information related to hot asset allocation.

Update your internal tracking of Section 751 exchanges —

especially those that occur late in the calendar year.

Coordinate with tax preparers to support accurate Form 1065

attachments for timely IRS filing.

For firms handling multiple transfers or with tiered partnership

structures, proactive tracking will be key to avoiding penalties

and back-end cleanup.

Your Path to Easier Year-End Reporting

MGO supports private companies navigating complex partnership

reporting obligations — including those related to Form 8308

and Section 751(a) exchanges. We help show which reporting applies,

streamline documentation, and provide guidance on both short-term

compliance and longer-term structure.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.