To print this article, all you need is to be registered or login on Mondaq.com.

Article Insights

Ankura Consulting Group LLC are most popular:

within Antitrust/Competition Law, Insolvency/Bankruptcy/Re-Structuring and Compliance topic(s)

Fraud Risk, the Failure to Prevent Fraud and the

Consequences of What Auditors Find

Recent enforcement signals from UK regulators have made one

thing clear: Fraud risk, and how organisations identify, assess,

and respond to it, is firmly back in the spotlight. Public

statements from the Serious Fraud Office (SFO) throughout 2025

confirm that the Economic Crime and Corporate Transparency Act

(ECCTA) and the new Failure to Prevent Fraud (FTPF) offence are

active enforcement priorities. Prosecutors are increasingly focused

on whether companies can demonstrate they have taken reasonable

steps to understand and mitigate fraud risk, including across

complex third-party relationships.

Against that backdrop, statutory audits are emerging as a

critical and often underestimated pressure point. Auditors are

required to assess fraud risk and internal controls as part of

their audit opinion. Where issues are identified, the audit process

can quickly escalate into deeper scrutiny, formal investigations,

and disclosures that may attract the attention of regulators,

lenders, and litigants alike.

This two-part series explores the growing intersection between

statutory audit, fraud risk, and ECCTA/FTPF exposure. Part one

examined how audit findings and auditor reporting can create

visibility and risk under the FTPF, often before misconduct is

fully understood. If you missed this article, you can access it here. Part two looks through the

auditor’s lens, explaining how fraud risk is evaluated in

practice, why audit-triggered investigations arise, and how their

outcomes can materially affect audit opinions, timelines, and

regulatory exposure.

Part 2: Fraud Risk and FTPF Through the Auditor’s Lens

When fraud risk surfaces during a statutory audit, the

consequences are rarely confined to a single audit procedure or

reporting period. Auditor concerns about fraud, management

integrity, or control effectiveness directly shape the scope,

depth, and duration of the audit; and can trigger formal

investigations, the outcomes of which determine not only the audit

opinion, but the company’s broader regulatory and litigation

risk. Understanding how auditors evaluate fraud risk in practice,

and why “reasonable assurance” can expand rapidly in

high-risk situations, is critical for boards and management

navigating audit scrutiny.

The Basics

Contrary to popular belief, the purpose of an audit is not to

identify fraud. The purpose of an audit is to obtain reasonable

assurance that the financial statements are free from material

misstatement, whether due to fraud or error.

Importantly, auditors must also consider whether the financial

statements, taken as a whole, could present a fraudulent

misrepresentation; that is, whether the overall portrayal of the

company’s performance or position is misleading, even if no

single line item is materially misstated.

Reasonable assurance

When supporting companies through investigations under audit

scrutiny, we often get questions like: “Is it reasonable for

the auditor to ask for this information?” or “How much

more testing do they need to do to get comfortable?” The

answer depends on the circumstances but is always tied to the fact

that reasonableness is a subjective measure determined by the

auditor.

Auditing standards define reasonable assurance as high, but not

absolute assurance that the financial statements as a whole are

free from material misstatement.1 In practice, this

means that audits are designed to reduce the overall audit risk

— i.e. risk the audit fails to detect material misstatements

— to an acceptably low level based on the auditor’s own

risk tolerance, but not to eliminate it entirely. There are

inherent limitations in an audit, such as the auditor’s use of

judgement, sampling techniques or the concealment of fraud, which

mean it is not possible to mitigate audit risk to zero, hence the

assurance being reasonable and not absolute.

Situations in which the auditor is concerned about fraud,

management integrity, or both, one can expect the bar for what is

reasonable to be significantly elevated.

Materiality

Materiality is another subjective measure. It is a financial

reporting concept that considers an assertion or omission to be

material if it can be reasonably expected to influence the economic

decisions of the users of the financial statements. When planning

and performing the audit, and when considering whether a

misstatement is material, the International Standards on Auditing

(ISA) 320 defers to the professional judgement of the auditor who

should consider how users of the financial statements would rely on

the information.2

There are scenarios in which the nature and scale of fraudulent

activity would not meet the definition of “material” in

this context. Even if financially significant to a particular

business unit, the auditor might consider the control environment,

likelihood of the risk being pervasive, and rule that so long as

the financial impacts have been rectified in the books and records,

that it is not material to the overall organisation’s financial

reporting. An example of this might be a conflict of interest that

transpires into an isolated procurement fraud with a particular

individual.

However, it is important to note that materiality is also

qualitative in nature. If audit procedures identify fraud concerns

in which there is suspected involvement from management; even if

the value is financially immaterial at a global level; it is likely

the auditor will have additional questions, want to perform

additional procedures, or even trigger an investigation. This is

because the auditor relies on various assertions by management,

both implicit and explicit, in the preparation and presentation of

the financial statements. If reliability in management is called

into question, there are significant impacts to how the auditor

approaches the remainder of the audit.

How Does the Audit Address Fraud Risk?

This is a perennial challenge and consistent expectation gap

between the public and the audit profession. It is important to

recognise the limitations of a statutory audit in this regard.

Fraud involving collusion, sophisticated concealments, or

management override can be difficult to detect.

ISA 240,”The Auditor’s Responsibilities Relating to

Fraud in an Audit of Financial Statements,” requires auditors

to design and perform procedures to identify and assess the risk of

material misstatement due to fraud. This includes assessing

relevant control frameworks and whether the auditor can rely on

those controls in designing their audit testing.3

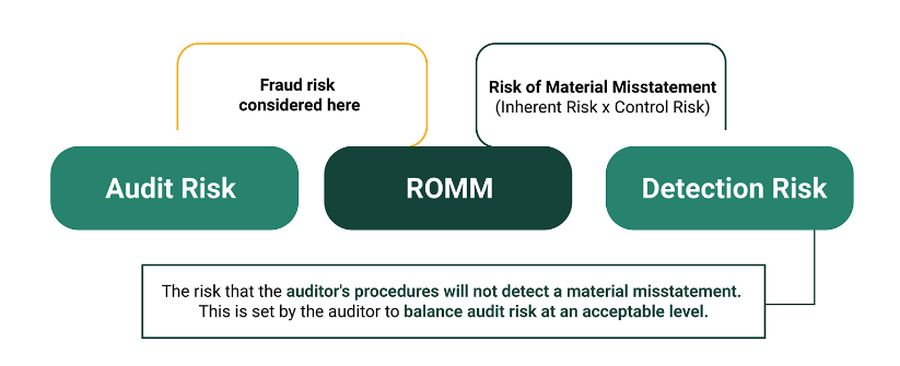

As discussed above, the auditor manages the risk that they fail

to identify misstatement — whether due to fraud or error

— referred to as “audit risk,” through a simple

equation. The interplay of the equation components is important to

understanding how fraud risk impacts the overall audit.

The only factor within the audit risk equation that is in the

auditor’s control is their detection risk. The discovery of

fraud or material weaknesses/gaps in fraud controls or issues with

management integrity during routine audit procedures will cause the

risk of material misstatement to increase. To account for this, the

auditor will enhance their testing to bring detection risk lower

and reduce overall audit risk to an acceptable level based on what

they will determine to be reasonable under the reasonable assurance

definition discussed above.

Notably, these enhanced procedures can include requesting that

the company commission an investigation and conducting their own

“shadow” investigation.

How Investigations Impact the Audit Process

When potential misconduct or irregularities surface during the

audit, the auditor’s work in that area typically pauses until

the matter is investigated and the facts are established. In such

circumstances, the auditor will often request that management

commission an investigation — either internally or with

external legal and forensic support — to determine the

nature, extent, and financial reporting impact of the issue.

Shadow Investigations

At the same time, auditors will frequently conduct their own

parallel review, often referred to as a shadow investigation, using

their internal forensic specialists. The purpose of this shadow

investigation is not to replicate the company’s inquiry, but to

evaluate its independence, scope, methodology, and evidential

quality, ensuring the findings can be relied upon as audit

evidence. Auditors must be satisfied that the investigation was

conducted objectively and that its conclusions are consistent with

the financial statements.

Extended Audit Timetable

While the investigation is underway, the auditor’s testing

in the affected areas is generally suspended. Once the

investigation concludes or reaches a stage where its findings are

sufficiently clear, the auditor will resume testing, typically

performing expanded audit procedures to obtain additional assurance

and bring the overall audit risk back to an acceptable level. This

may include reperforming certain tests, corroborating findings with

independent evidence, or extending the scope of substantive

procedures.

These dynamics almost invariably extend the audit timetable. The

additional investigative steps, verification procedures, and

internal consultations required to reach a supportable opinion can

significantly delay the issuance of the audit report. This often

becomes a point of tension between management, the board, and the

auditors, particularly where reporting deadlines, market

expectations, or regulatory filing obligations are approaching.

How Outcomes from Investigations Impact the Audit Opinion

Once the investigation concludes and additional procedures were

performed, the auditor determines how the findings affect the audit

opinion. The impact depends on the severity, pervasiveness, and

evidential support of the findings:

Unmodified Opinion With Emphasis of Matter: The issue is

resolved but significant enough to warrant highlighting to users of

the financial statements.

Qualified Opinion: Misstatement or limitation of scope exists

but is confined to specific elements or areas.

Adverse Opinion: Misstatements are material and pervasive,

meaning the financial statements, as a whole, are misleading.

Disclaimer of Opinion: The auditor is unable to obtain

sufficient evidence to form an opinion; this is typically where

management restricts access or investigations remain

incomplete.

A more extreme outcome is auditor resignation, typically when

the auditor no longer has confidence in management integrity or

access to information. Such events are rare but carry significant

reputational and regulatory consequences.

Even where the final opinion is not modified, investigation

outcomes may drive new management letter points, control

recommendations, or required disclosures under ISA 265:

“Communicating Deficiencies in Internal Control.”

Navigating the Risks

Where audits and investigations run concurrently, the stakes are

high. Modified opinions, delayed filings, and auditor resignations

carry immediate market, financing, and reputational consequences.

Audit disclosures can also draw regulatory attention to potential

FTPF or broader ECCTA exposure, even in the absence of

self-reporting, and may act as a catalyst for follow-on litigation

or shareholder action.

Despite commonly feeling held hostage by the audit process,

there are ways for the board and management to regain control.

Auditors are required to communicate significant findings from the

audit, including throughout the audit process and before the audit

report is issued. This provides an opportunity for the board to

commission its own review of concerning conduct and enable them to

interact with the auditors from a place of confidence and

understanding of the issues. It also provides the board a headstart

in remediating control issues that create ECCTA/FTPF risks before

the audit report makes those issues public to prosecuting

authorities.

In this environment, boards and audit committees benefit from

experienced, independent support that understands both the audit

process and investigative expectations. Ankura’s forensic

accounting and investigations specialists regularly assist

organisations and their advisers in responding to audit-driven

fraud concerns, conducting defensible investigations under intense

scrutiny, and managing the interaction between auditors,

regulators, and other stakeholders. Our experience advising

corporates, audit firms, and audit regulators allows us to

anticipate how audit and investigation findings will be tested,

challenged, and ultimately reflected in the audit opinion —

helping clients maintain control of the process at moments when it

matters most.

Footnotes

3. https://media.frc.org.uk/documents/ISA_UK_240_Revised_May_2021_Updated_September_2025.pdf

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.