As a two-year consumer and liquidity-fueled boom petered out in 2025, the economy has transitioned into a complex mix of resilience and stagnation.

Sep. 3, 2025: Managing sanctions and trade flows in recent years has become ever more complicated for the Kremlin leader, Vladimir Putin. © Getty Images

Sep. 3, 2025: Managing sanctions and trade flows in recent years has become ever more complicated for the Kremlin leader, Vladimir Putin. © Getty Images

×In a nutshell

Russian household spending is quashed by high interest rates

Low investment and military focus hit the industrial sector

Asian supply chains are key to overseas trade growth

For comprehensive insights, tune into our AI-powered podcast here

The Russian economy in 2025 presented a complex picture in which resilience and fragility coexisted. This was in spite of the Western sanctions-induced economic shock the country faced following its 2022 invasion of Ukraine, albeit supported by an unexpected economic rebound in 2023 and 2024.

Official data indicate that gross domestic product (GDP) expanded by 4.1 percent in both years, a performance that surprised many external observers. Yet the forces behind this expansion were far from typical for a peacetime, market-oriented economy. Instead, Russia entered what has frequently been described as a “war economy,” in which state spending – especially on the military-industrial complex – became the primary engine of growth.

Within this unusual environment, Russia also witnessed what many have termed a domestic consumer boom. This was driven not by structural improvements in productivity or market conditions, but by rising wages and state transfers linked directly to the war effort.

Temporary Russian liquidity boom

During the Covid-19 pandemic from 2020 to 2021, and again from the start of its invasion of Ukraine in 2022, a visible shift emerged in flows of financial capital: Russians increasingly moved assets previously held abroad back into domestic banks. For instance, recent data show monthly net transfers into domestic accounts of 58.5 billion rubles ($756 million) in August 2025 – matching the previous high recorded in March of that year.

Amid global economic uncertainty and domestic regulatory tightening, the trend marked a notable reversal in the behavior of Russian households and investors who used to send capital overseas, mainly to offshore “safe haven” jurisdictions in the Americas and Europe.

A visible shift emerged in flows of financial capital: Russians increasingly moved assets previously held abroad back into domestic banks.

This repatriation of capital contributed to a replenishment of liquidity in the domestic banking sector and the economy more broadly. According to data from the Central Bank of Russia, by the end of 2023 the credit that banking systems extended to households and firms rose by 22.9 percent, sharply up from 12 percent growth in 2022; with foreign-currency credit also rising strongly. The expansion in domestic banks’ balance sheets helped fuel a surge in lending: with mortgage, consumer car loans and unsecured consumer credit all growing quickly.

Concurrently, the broad money supply expanded rapidly. According to one estimate, M2 (highly liquid, readily available money comprising notes, coins in circulation and current account deposits held with banks), doubled from roughly 62 trillion rubles ($801.5 billion) in December 2021 to 118 trillion in early 2025. Accordingly, the share of M2 in GDP rose from 46 percent to 56 percent over that period.

This repatriation of capital contributed to a replenishment of liquidity in the domestic banking sector and the economy more broadly.

This increase in money supply, combined with renewed bank lending, helped channel repatriated capital – alongside newly created domestic liquidity (ruble issuance and credit expansion) – into the real economy. These trends supported consumption and some investment, even in a context of external sanctions and trade disruption.

The result of the state spending, household and investor repatriation of assets and resumption of lending fueled a significant surge in domestic demand, especially in 2023 and 2024. This contributed significantly to annual growth rates exceeding 4 percent during that period.

Fossil-fuel deposits and exports are central factors bolstering the resilience of the Russian economy despite external pressures. The International Monetary Fund (IMF) and the World Bank ranked Russia as the world’s fourth largest economy in terms of purchasing power parity in 2025 and 2023-2024, respectively.

Mixed picture of industrial growth

Much of the impetus behind the 2023-2024 rebound came not only from a surge in private consumption but also from massive state spending. Defense-sector activity and state procurement orders expanded dramatically, pulling industrial output upward, primarily in sectors tied to weapons manufacturing, logistics and military supplies.

As labor markets tightened – due to both conscription and an increasing demand for workers in defense-related industries – real wages rose rapidly, particularly for those employed in or adjacent to the military-industrial complex. In addition, payments to soldiers and their families injected significant disposable income into specific regions and demographic groups, further fueling a rise in overall household consumption. The Bank of Russia itself noted this dynamic, raising its 2024 consumption growth forecast to the 4-5 percent range.

Although this consumption surge appeared vibrant in statistical terms, it was not evenly distributed across the population. Families benefiting from military employment or state-linked sectors enjoyed rising incomes, while many small and medium-sized businesses struggled under the weight of sanctions, rising borrowing costs and disrupted supply chains.

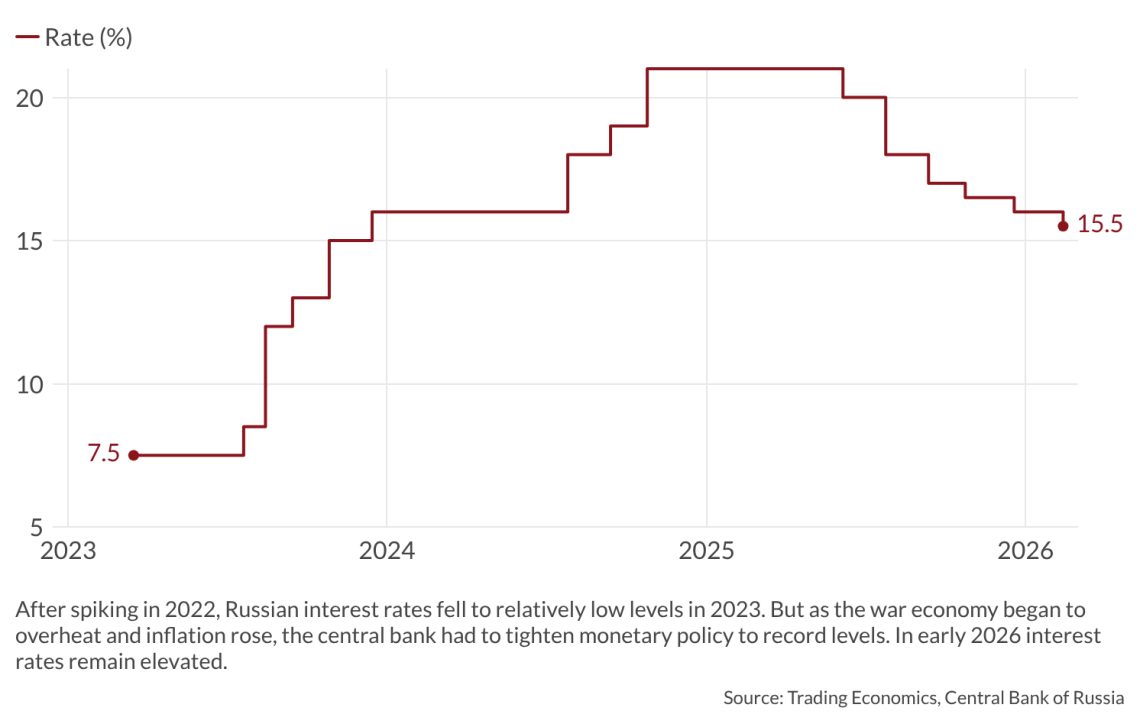

Furthermore, inflation began to accelerate as supply constraints met rising demand. By 2024, consumer price inflation reached nearly 10 percent, pressuring households outside state-influenced sectors and prompting Russia’s central bank to sharply tighten monetary policy. The central bank raised its headline interest rate to 21 percent in 2024, the highest level in years, making credit expensive and placing further strain on private-sector investment. Investment conditions remain difficult. While the central bank lowered rates somewhat in 2025, the headline rate remained significantly elevated at 16 percent in early 2026, discouraging private borrowing for expansion, modernization or long-term projects.

×Facts & figures

Russian interest rates remain at elevated levels

State-directed investment continues, but it increasingly prioritizes military production and related infrastructure rather than diversified civilian sectors. Many firms, especially small and medium-sized ones, face uncertain returns. The result is a pattern of low investment that gradually erodes the capital stock and reduces productive capacity.

Over the course of 2025, the sustainability of the consumer boom of the previous two years became increasingly doubtful. Inflationary pressures, high interest rates and the exhaustion of the initial wartime stimulus all pointed toward a slowdown.

×Facts & figures

Russian economic growth slowing to near stagnation

Early 2025 data confirmed this shift: GDP in the first three quarters of the year showed a persistent decline, falling from an annual pace of 1.4 percent in Q1 to 0.6 percent in Q3 – a stark contrast to the previous year’s performance. Government forecasts were revised downward, with the finance ministry reducing its expected full-year 2025 growth rate from 2.5 percent to 1.5 percent, while the IMF adopted an even more pessimistic view, predicting growth of only 0.6 percent. In February 2026, Russian President Vladimir Putin said that GDP growth for the entire year of 2025 was only 1 percent.

This data highlights the waning momentum of the wartime economy as well as the challenges posed by tight credit conditions and slowing consumption.

Asia-oriented supply chains sustain trade

In light of domestic pressures, Russia’s external trade has remained an essential – if diminishing – source of stability. The country’s current-account surplus is significantly smaller than it was a year earlier; in the first three quarters of 2025, it fell to approximately $30 billion from over $49 billion in the same period of 2024.

The narrowing surplus reflected falling export revenues, especially in the oil and gas sectors, while import volumes have proven stable. August 2025 data showed a monthly trade surplus of $7.47 billion, down from $8.65 billion the year before.

Structurally, one of the most dramatic shifts in Russia’s external economic relations since 2022 has been its reorientation away from Europe and toward Asia, particularly China. By 2025, China had become Russia’s main trading partner for both exports and imports; roughly a third of Russia’s exports go to China, and more than a third of its imports come from Chinese producers. This effectively replaces its former volume of trade with the European Union. Now only around 8 percent of its exports go to the EU, a remarkable drop from prewar levels.

Sep. 3, 2025: Mr. Putin speaks while visiting Beijing to bolster Russia’s engagement with China. © Getty Images

Sep. 3, 2025: Mr. Putin speaks while visiting Beijing to bolster Russia’s engagement with China. © Getty Images

In contrast, India, Turkiye, countries in the Middle East and various states in Central and South Asia are becoming far more important as trading partners. This reorientation is needed so that Russia can continue to ship its goods abroad and obtain the consumer and industrial products it needs.

However, the new trade patterns come with costs. Asian buyers, when willing to purchase Russian oil, gas and minerals, usually do so at discounted prices. As a result, while export volumes in 2025 remained relatively high, revenue per barrel or ton was much lower than before, and no change is expected. The loss of European markets deprives Russia of buyers who traditionally paid higher prices and were deeply integrated in its pipeline infrastructure.

Russia’s export situation worsened in late 2025 and at the start of 2026, when the United States began seizing tankers it believed were part of Russia’s sanctions-evading shadow fleet. Washington has also agreed with New Delhi on a trade deal, lowering tariffs on Indian goods in return for India sharply reducing its purchases of Russian oil, according to U.S. President Donald Trump.

However, Indian officials are not forthcoming when questioned about oil purchases. India’s trade minister, Piyush Goyal, has said the deal “does not decide who buys what and from where” and no joint statement was issued confirming this arrangement. External affairs ministry spokesman Randhir Jaiswal, when recently asked if India was cutting oil purchase from Russia, did not deny it.

Beyond this uncertainty, Russia faces logistical challenges to sustain exports: longer shipping routes, higher transportation costs, limited access to Western insurance and ongoing risks due to drone attacks on refineries and energy facilities.

Deteriorating yet manageable fiscal space

In 2025, the Russian government faced growing fiscal stress as it increased spending sharply – especially on defense and national security – while revenues were squeezed by weak energy receipts. The latest official projections put the 2025 federal budget deficit at between 1.7 percent of GDP and, under some draft amendments, as high as 2.6 percent.

Expenditures have been revised upward by roughly 830 billion rubles ($10.6 billion), while revenues – mainly from oil and gas – have been revised downward substantially, reflecting expectations of prolonged low global energy prices, the possible loss of significant Indian purchases and existing sanctions constraints.

Defense and security together consume as much as 40 percent of total federal expenditure – far outstripping allocations for social programs, health and education.

A central feature of the 2025 budget is the dramatic expansion of defense spending, set to reach approximately 6.3 percent of GDP, with allocations totaling 13.5 trillion rubles ($175 billion), the largest share since the Cold War. Defense and security together consume as much as 40 percent of total federal expenditure – far outstripping allocations for social programs, health and education.

To shore up the shortfall, the government plans to draw on liquid fiscal reserves and has already initiated a range of measures. Russia raised corporate taxes at the start of 2025 from 20 to 25 percent. Mid-year, the finance ministry announced it would tap some 447 billion rubles from the national wealth fund, and in January 2026 the country increased value-added tax to 22 percent. President Putin has also voiced support for introducing a wealth tax or higher taxes on dividends.

Read more by trade and sanctions expert Bob Savic

This fiscal strategy has mixed effects on the economy. In the short run, increased state spending – especially on defense orders, military wages and procurement – injects liquidity and demand into certain sectors, helping sustain parts of industrial output, wages and employment. But the heavy tilt toward military and security spending means that much of the budget is diverted from civilian investment, social infrastructure or long-term development projects.

In terms of sustainability, Russia’s relatively low public debt (as a share of GDP) gives the government some fiscal space to run moderate deficits, yet this tolerance has limits. Continued reliance on volatile commodity revenues, a tight external environment and falling oil and gas income erode that buffer. As energy revenues shrink, the pressure to maintain military spending and social transfer commitments may force further draws on reserves, still higher taxation or increased domestic borrowing. If global energy prices remain low or external demand for Russian exports weakens, the deficit could widen further, raising the risk for fiscal stability.

So, while the budget may be manageable in the short term, Russia’s long-term fiscal sustainability looks increasingly fragile unless Moscow significantly diversifies its revenue base or reduces its military and security burdens.

×

Scenarios

Less likely: Russian economic collapse

A convergence of adverse conditions including falling commodity prices, new sanctions on logistics or maritime services, disruptions to energy infrastructure or escalating war expenditures could lead to severe economic distress.

Under such circumstances, Russia’s export revenues could fall significantly, undermining the trade surplus and further straining public finances. Budget deficits could widen, prompting cuts to social spending or increases in domestic borrowing. Consumption and investment would likely contract, unemployment might rise and living standards could decline more visibly.

Although this scenario does not necessarily unfold into an immediate or dramatic economic collapse, it suggests the possibility of a prolonged period of economic decline and social stress.

More likely in the medium term: Low but stable economic growth

For the period between 2026 and 2028, Russia’s economy is likely to maintain macroeconomic stability, avoiding excessive inflation and keeping its external accounts positive, but it will remain stuck in a low-growth trajectory.

Its ability to escape this dynamic is limited by a political environment that prioritizes military spending and centralized control over innovation, openness and efficiency. The consumer and banking sector liquidity boom of 2023-2024 has ended, and the economy is returning to a more subdued consumption pattern shaped by slower wage growth, higher borrowing costs and persistent inflationary pressures. These domestic and external dynamics combine to produce a medium-term economic outlook characterized by slowing growth and structural constraints.

Russia increasingly looks to be entering a period of “managed stagnation,” in which the economy neither collapses nor recovers robustly but instead stabilizes at a lower baseline. In this context, growth over the next few years is likely to hover between 1 and 2 percent annually under normal conditions, though it may edge higher during periods of strong commodity prices or decline during periods of global economic weakness.

The productivity of many non-military sector industries is also likely to decline over time. This is exacerbated by Russia’s weakening human capital base, given hundreds of thousands of skilled workers, professionals and entrepreneurs have emigrated or withdrawn from economic activity since 2022. Combined with an aging population and a war-driven decline in available labor, this reduces long-term growth potential.

Despite these challenges, Russia retains a degree of resilience, largely due to its natural-resource endowments and its ability to sustain trade flows with non-Western partners.

In a favorable external environment – characterized by high commodity prices and strong demand from China, India and likely other Global Majority economies – Russia could maintain growth in the 2-3 percent range for several years. Such an outcome would allow the state to sustain social transfers, military spending and limited industrial investment, stabilizing living standards and preserving internal political cohesion.

However, this outcome is highly dependent on factors beyond Russia’s control, such as global energy markets and the policies of major Asian importers, especially India.

Most likely: Moscow continues walking a tightrope to sustain the status quo

Several indicators will be crucial for understanding Russia’s future trajectory. These include global commodity prices, the evolution of trade relationships with China and other non-Western partners, the level of foreign-exchange inflows, the government’s fiscal position and the direction of central bank policy.

Domestic factors such as the pace of emigration, the condition of civilian industries, and the state’s ability to maintain or expand social support will also play significant roles.

Above all, developments in the Kremlin’s war on Ukraine and Russia’s economic isolation from the West will remain key issues shaping the fundamental constraints under which the economy operates. These include whether a peace deal brokered by President Trump will be accepted by Russia and Ukraine, with the latter under extreme pressure from Washington.

Contact us today for tailored geopolitical insights and industry-specific advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.