United States Antimony (UAMY) shares are in focus after the company entered a joint venture with Americas Gold and Silver to build and operate an antimony processing plant in Idaho’s Silver Valley.

See our latest analysis for United States Antimony.

The joint venture news comes after a volatile period, with the share price at US$7.39. A 30 day share price return of a 31.89% decline contrasts with a 90 day gain of 25.68% and a very large 1 year total shareholder return. This suggests that momentum has cooled recently after a powerful longer term move.

If this antimony supply chain story has your attention, it could be a good moment to look across the materials space and check out 25 elite gold producer stocks as potential next ideas.

With the share price pulling back over the last month, yet still sitting on a very large 1 year total return and trading below one analyst price target, you have to ask yourself: is there real value here, or is the market already pricing in future growth?

Most Popular Narrative: 32.3% Undervalued

United States Antimony’s most followed narrative pegs fair value at $10.92, which sits well above the recent $7.39 close, and builds a case around growth, capacity and policy support.

US Antimony is expanding its domestic processing capacity (for example, a sixfold increase at the Thompson Falls facility expected by year end) and increasing ore supply both from its own Montana/Alaska projects and multiple new international sources, which, if achieved, would support higher production volumes and revenue through increased throughput and supply security.

Curious what kind of revenue ramp and margin profile would justify that higher fair value, plus an increased future earnings multiple, even while shares have been volatile recently? The full narrative outlines the growth curve, profitability shift and valuation bridge that would need to align to support that $10.92 figure.

Result: Fair Value of $10.92 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, you should also weigh the risk that permitting setbacks at Alaska and Ontario projects, or extended supply chain issues, could hold back the growth story that investors are watching.

Find out about the key risks to this United States Antimony narrative.

Another Angle on Valuation

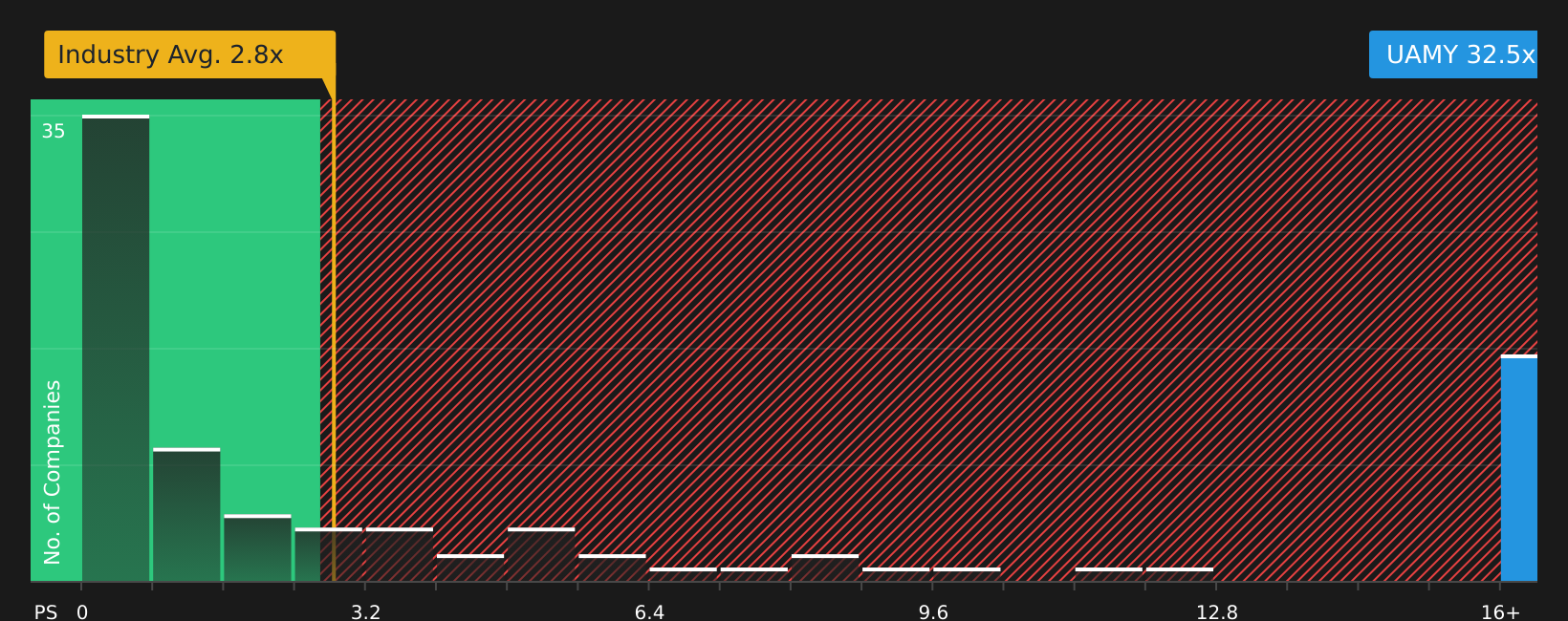

Those fair value models paint UAMY as 14% below our estimate, but the market is also charging a steep P/S of 32.5x, versus 7x for peers and 2.8x for the wider US Metals and Mining industry. With our fair ratio at 2.9x, is enthusiasm running ahead of fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

NYSEAM:UAMY P/S Ratio as at Feb 2026Next Steps

NYSEAM:UAMY P/S Ratio as at Feb 2026Next Steps

If this mix of optimism and concern feels familiar, do not wait on others to decide the story for you. Instead, check the 2 key rewards and 2 important warning signs and judge the balance yourself.

Looking for more investment ideas?

If you are serious about building a watchlist that matches your goals, do not stop at a single stock story. Let the data point you to your next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com