For federal retirees, few issues generate as much anxiety as Medicare’s Income-Related Monthly Adjustment Amount (IRMAA). The instinctive response is simple: avoid it at all costs. Yet for many retirees under the Federal Employees Retirement System (FERS), that instinct can quietly increase lifetime taxes—especially once Required Minimum Distributions (RMDs) and survivor tax rules come into play.

When IRMAA cannot be avoided entirely, the real planning question is not whether to pay it, but whether paying a temporary Medicare surcharge today can reduce permanent taxes tomorrow.

IRMAA applies to Medicare Parts B and D and is calculated by the Social Security Administration using Modified Adjusted Gross Income (MAGI) from two years prior. For federal retirees, MAGI often includes a combination of FERS pension income, Thrift Savings Plan (TSP) withdrawals or Roth conversions, taxable Social Security benefits, and investment income. The presence of a guaranteed pension alongside a large pre-tax TSP balance makes federal retirees especially vulnerable to IRMAA later in retirement.

IRMAA vs. RMDs: A Tradeoff Often Missed

Avoiding IRMAA frequently means avoiding Roth conversions. While that may feel prudent, the long-term consequences can be significant.

Skipping conversions can lead to larger RMDs starting at age 73, higher marginal tax brackets later in retirement, and repeated IRMAA exposure rather than a limited, controlled surcharge. Perhaps most importantly, it can magnify tax compression for the surviving spouse.

The key distinction is straightforward: IRMAA is temporary. RMDs—and survivor taxes—are not.

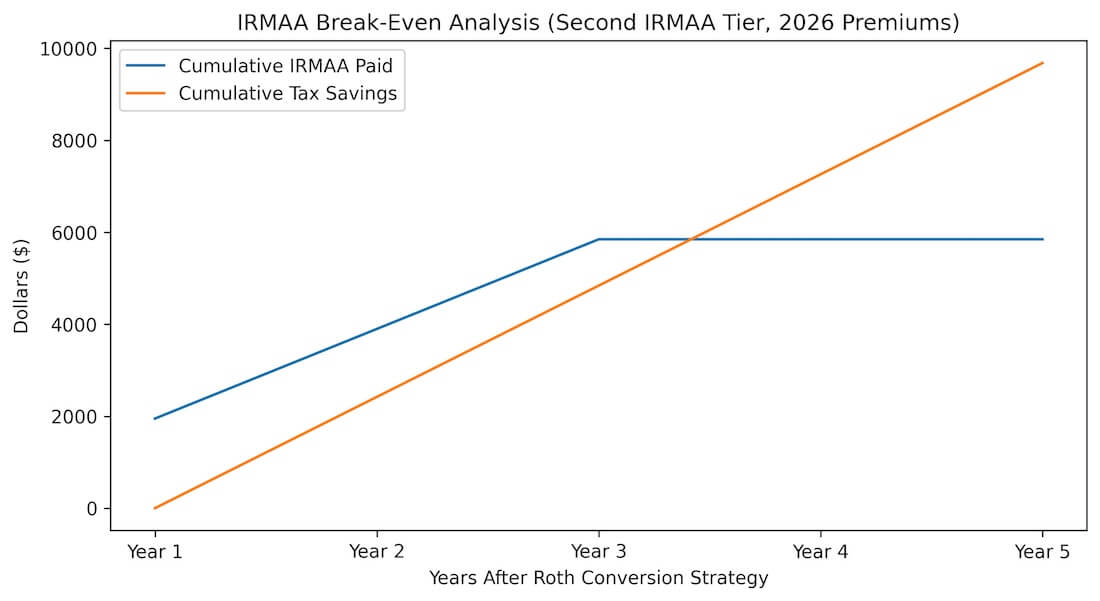

Consider a married FERS retiree household, both age 65, filing jointly. The couple receives a $42,000 FERS pension and $38,000 in combined Social Security benefits. They hold $1.2 million in a Traditional TSP and complete Roth conversions of $100,000 per year for three years. During the conversion years, their marginal tax rate is 22 percent.

A $100,000 annual conversion pushes the couple from the first IRMAA tier to the second tier. The 2026 IRMAA premiums show that the first IRMAA tier adds $0.00 per month per person to the basic premium. The second tier, however, is an additional $81.20 per month per person. This would be $974.40 per person, or $1,948.80 for the couple’s annual, added to the first-tier premium. Let’s round it up to $1,949 per year. After three years, the total costs would be $5,847.

In return, the couple moves $300,000 out of the future RMD system. This reduces lifetime taxable income, lowers the likelihood of IRMAA in later retirement, and increases flexibility for income planning—especially for the surviving spouse.

Break-Even Math

Without Roth conversions, the first RMD at age 73 on a $1.2 million TSP is approximately $45,000. That distribution is taxed every year, often at rates between 22 and 24 percent, and it increases future IRMAA and survivor tax exposure.

With Roth conversions, the TSP balance is reduced to roughly $900,000, producing an RMD of about $34,000. That is an annual reduction of approximately $11,000.

At a 22 percent tax rate, annual tax savings are about $2,420. Dividing the total IRMAA paid ($5,847) by those annual savings produces a break-even point of roughly 2.4 years. Beyond that point, the Roth strategy delivers ongoing annual savings.

IRMAA Break-Even Analysis Using 2026 Second-Tier Premiums

IRMAA Break-Even Analysis Using 2026 Second-Tier Premiums

Although Roth conversions trigger temporary Medicare IRMAA surcharges, the reduction in future RMD-driven taxes can exceed the IRMAA cost within a few years. After the break-even point, the strategy produces ongoing annual tax savings and improved flexibility for surviving spouses.

The Silent Risk: The First Death

This is where Roth conversions often provide their greatest value.

When one spouse dies, filing status typically shifts from Married Filing Jointly to Single. Tax brackets compress sharply, while IRMAA thresholds remain unchanged. RMDs often stay nearly the same because account balances remain substantial.

As a result, surviving spouses can be pushed into higher marginal tax brackets, permanent IRMAA surcharges, and reduced flexibility in managing withdrawals. In many FERS households, the survivor—not the retiree—ultimately pays the highest lifetime tax bill.

Roth assets help mitigate this risk. Roth withdrawals do not increase MAGI, do not trigger IRMAA, and allow survivors to manage cash flow without compounding tax and Medicare costs.

When Paying IRMAA Makes Sense

Paying IRMAA can be financially sound when income spikes are temporary, Roth conversions materially reduce future RMDs, survivor tax compression is a concern, or IRMAA is likely to occur later regardless. The objective is not avoiding IRMAA forever, but shortening and controlling it.

For many federal retirees, the most expensive strategy is successfully avoiding IRMAA today—only to face higher taxes, higher Medicare premiums, and higher survivor costs for decades afterward.

© 2026 Francis Xavier (FX) Bergmeister. All rights reserved. This article

may not be reproduced without express written consent from Francis Xavier (FX) Bergmeister.