Report Overview

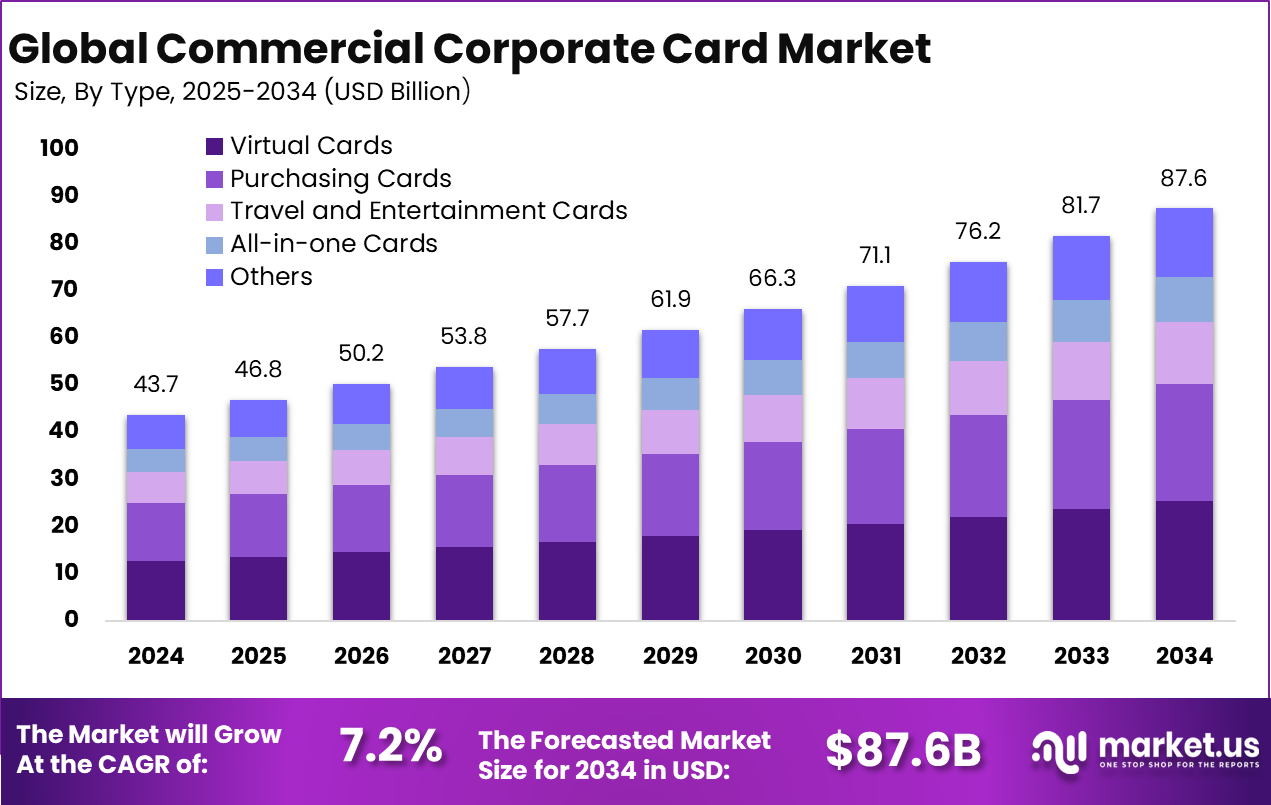

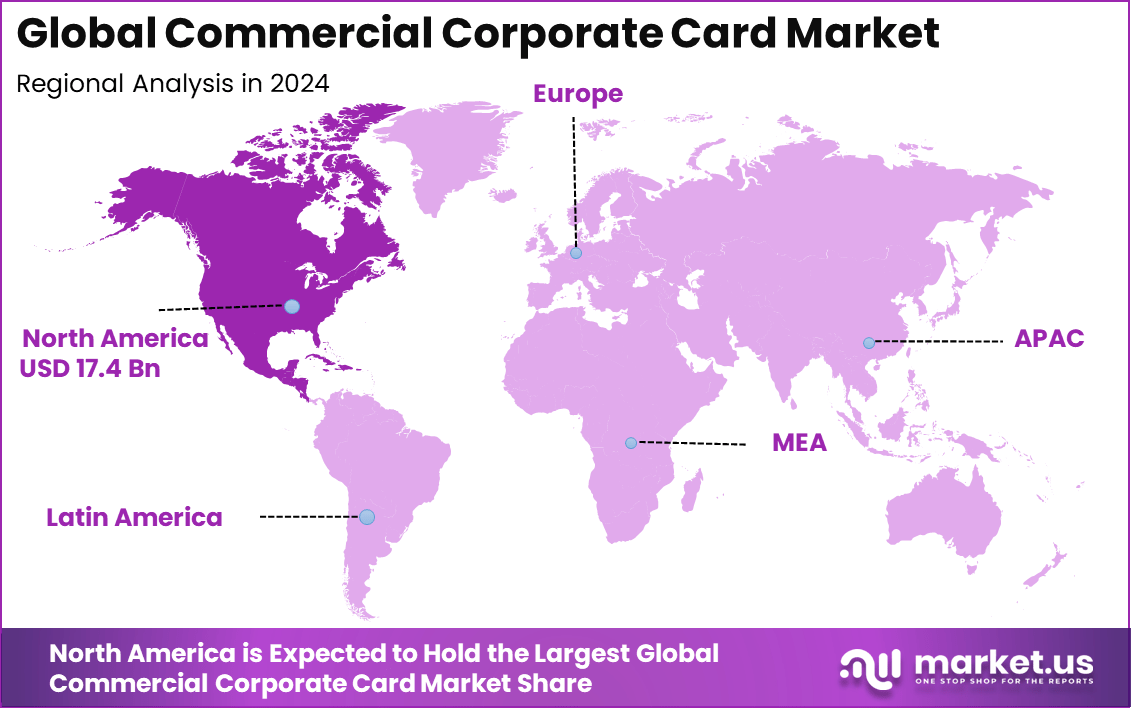

The Global Commercial Corporate Card Market size is expected to be worth around USD 87.6 billion by 2034, from USD 43.7 billion in 2024, growing at a CAGR of 7.2% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 40% share, holding USD 17.4 billion in revenue.

The commercial corporate card market comprises payment solutions specially designed for business expenses such as travel, procurement, and operational costs. These cards are integrated with expense management platforms to deliver detailed transaction visibility and support financial governance. Their use has grown significantly with digital transformation of enterprise finance systems.

The growth of this market is primarily driven by corporate digitalisation of financial processes and the need for automated expense control systems. The integration of card programs with accounting and ERP systems has delivered real‑time oversight, policy enforcement, and streamlined reconciliation, which have become core motivations for adoption.

According to study, In 2023, global commercial card spending surpassed $4 trillion for the first time, marking an 8% year-over-year growth. This figure is expected to exceed $6 trillion by 2029. The travel and entertainment (T&E) card segment led growth with a 16% increase, driven by rising travel demand and costs, particularly in emerging markets like India.

Small businesses contribute to over 35% of total B2B commercial card spending in the U.S., representing nearly $500 billion in transaction value. This highlights the increasing adoption of commercial cards among smaller enterprises, a trend likely to persist as digital payment systems become more widespread and essential to business operations.

For instance, In September 2023, IndusInd Bank introduced a virtual commercial credit card to support cross-border payments for corporates and travel agents. This solution enables secure, seamless international transactions and enhances global payment efficiency. It provides businesses with improved control, flexibility, and compliance with global financial standards.

Market Size and Growth

Demand analysis indicates strong interest from companies of all sizes, especially those expanding regionally and internationally. These businesses aim to simplify recurring purchases, travel expenses, and large procurement while reducing administrative tasks. The shift to online commerce and remote work further strengthens the global demand for commercial corporate cards, improving cash flow and vendor coordination.

Technology adoption is reshaping expense management. Tools such as virtual cards, mobile apps, instant payments, and biometric authentication are now widely used. These solutions enhance security, enable real-time tracking, integrate smoothly with accounting platforms, and offer advanced fraud protection, fostering greater trust and broader industry adoption.

Key Takeaway

The global commercial corporate card market is projected to reach USD 87.6 billion by 2034, growing from USD 43.7 billion in 2024, supported by a steady CAGR of 7.2% through the forecast period.

By type, virtual cards represent 29% of the market, showing a rising preference for secure, contactless, and digitally traceable payment solutions among businesses.

In terms of card design, open-loop cards dominate with a 70% share, suggesting strong demand for cards that are widely accepted and integrated across global networks.

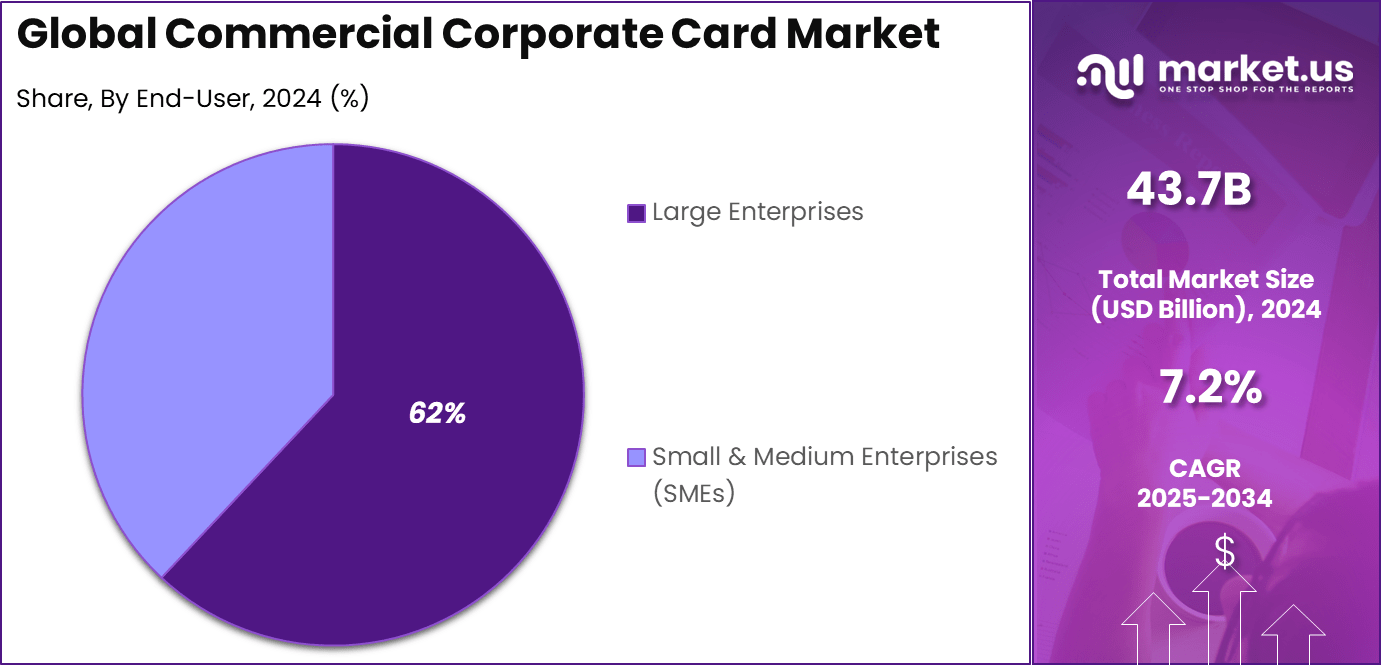

Large enterprises account for 62% of the end-user share, driven by the need for centralized control, real-time tracking, and improved visibility across large-scale financial operations.

North America leads the global landscape with over 40% market share in 2024, generating USD 17.4 billion in revenue, indicating strong regional adoption and corporate digital payment maturity.

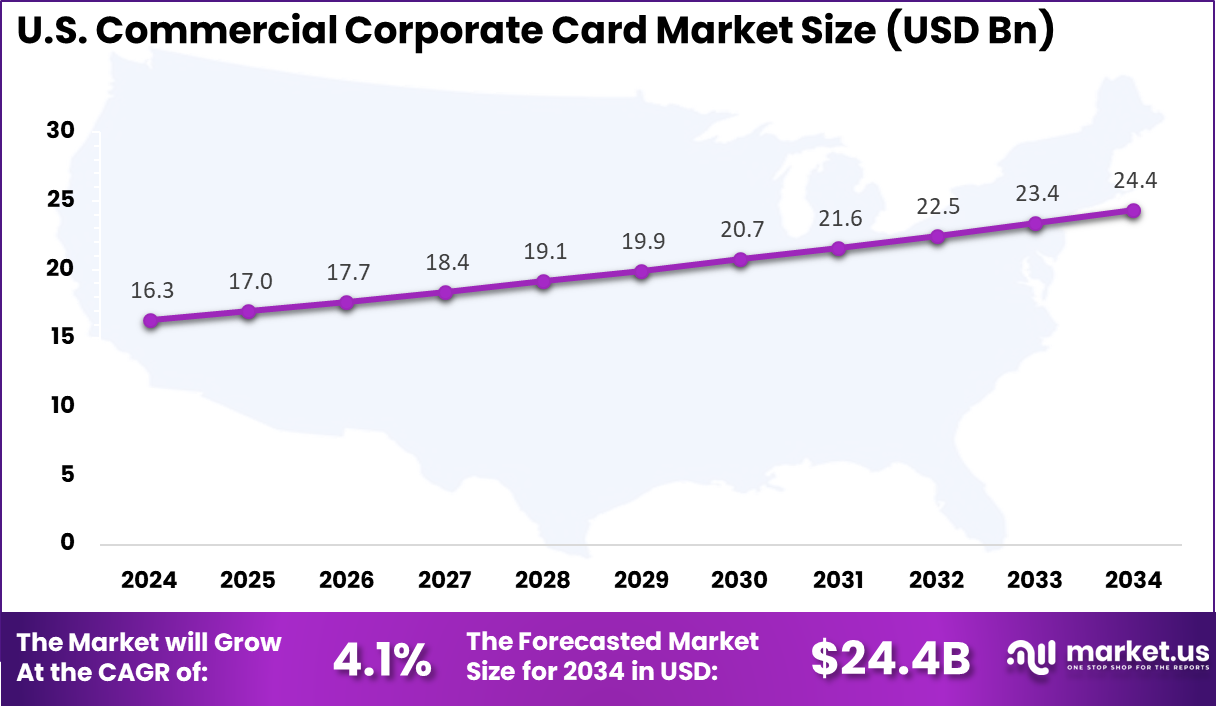

Within North America, the United States alone accounts for USD 16.3 billion, with a modest yet stable CAGR of 4.1%, reflecting consistent enterprise-level usage and innovation in expense management tools.

U.S. Market Outlook

The market for Commercial Corporate Card within the U.S. is growing tremendously and is currently valued at USD 16.3 billion, the market has a projected CAGR of 4.1%. This market is growing tremendously due to the increasing shift towards digital payment solutions, driven by the need for enhanced efficiency and transparency in business operations.

U.S. companies are increasingly adopting corporate cards to streamline expense management, improve financial control, and automate reporting. Additionally, the integration of these cards with advanced expense management software and corporate travel tools is appealing to businesses seeking to reduce administrative overhead and gain real-time insights into spending.

For instance, in June 2025, American Express announced major updates to its U.S. Consumer and Business Platinum Cards, set to launch later in the year. These enhancements will focus on expanding travel, dining, and lifestyle benefits, providing cardholders with more exclusive perks and greater flexibility. The updates aim to further differentiate the Platinum Card as a premium offering, enhancing its appeal to frequent travelers and business professionals.

In 2024, North America held a dominant market position in the Global Commercial Corporate Card Market, capturing more than a 40% share, holding USD 17.4 billion in revenue. This dominance is due to its well-established financial infrastructure, high adoption of digital payment solutions, and the presence of leading corporate card issuers.

The region’s businesses are increasingly leveraging corporate cards to streamline expense management, enhance financial control, and improve operational efficiency. The region’s robust financial ecosystem, characterized by leading financial institutions and innovative fintech solutions, supports seamless integration of corporate cards with expense management tools and corporate travel systems.

For instance, in March 2024, Regions Bank launched Visa Commercial Pay Mobile for its corporate banking clients, further solidifying North America’s dominance in the commercial corporate card market. This new solution provides businesses with enhanced flexibility and convenience by enabling mobile payments through a secure, digital platform.

Top 5 Growth Factors

Type Analysis

In 2024, the Virtual Cards segment held a dominant market position, capturing a 29% share of the Global Commercial Corporate Card Market. This dominance is driven by businesses increasingly adopting virtual cards for their superior security features, such as tokenized numbers, merchant-specific limits, and dynamic expiration dates, which help mitigate payment fraud.

Virtual cards also offer immediate advantages like fraud prevention, rebate opportunities, and accounts payable automation, making them appealing to enterprises. The growth of this segment is further fueled by the rise in online transactions, digital transformation, smartphone adoption, and seamless integration with financial systems, enabling better real-time payment and expense management.

For Instance, in February 2025, MTN MoMo Uganda introduced the Virtual Card by MoMo to drive e-commerce growth in the region. This innovative virtual card allows users to make secure online payments, providing a convenient and accessible solution for Ugandans engaging in digital commerce. By leveraging MTN’s mobile money platform, the virtual card enhances financial inclusion and supports the growing demand for e-commerce in Uganda.

Card Type Analysis

In 2024, the Open-loop Card segment held a dominant market position, capturing a 70% share of the Global Commercial Corporate Card Market. This segment is driven by their flexibility and widespread acceptance across global networks and merchants.

These cards, supported by major payment networks like Visa, Mastercard, and American Express, cater to businesses with diverse payment needs, including international transactions. The growing shift toward cashless and contactless payments, along with the seamless integration of open-loop cards into expense management and accounting systems, has further boosted their appeal.

For instance, In June 2025, Shuttel and Enfuce launched an open-loop mobility card to transform business travel in the Netherlands. This solution allows companies to manage transportation, lodging, and related expenses through one unified payment system, offering real-time tracking, improved flexibility, and stronger control over travel budgets.

End-User Analysis

In 2024, the Large Enterprises segment held a dominant market position, capturing a 62% share of the Global Commercial Corporate Card Market. This dominance is driven by the substantial and diverse spending needs of large enterprises across travel, procurement, and operations, leading to higher card usage and transaction volumes.

Corporate cards provide these businesses with improved control over expenses, real-time tracking, and streamlined reconciliation. Moreover, their ability to integrate seamlessly with enterprise resource planning (ERP) systems and expense management tools makes them an essential solution for managing complex financial operations across multiple departments and regions.

For Instance, in October 2024, Bank of America unveiled its Virtual Payables solution, specifically designed to support large enterprises in the booming B2B payments sector. This innovative platform allows businesses to make supplier payments via direct bank transfers while benefiting from the advantages of card transactions.

Drivers

Increasing Adoption of Digital Payments

The adoption of digital payments by businesses is making business credit cards an essential means of improving their operations. By supporting seamless transactions, integrating with expense management systems, and providing real-time reporting, corporate cards offer a secure and scalable solution.

This shift to digital payment systems helps businesses streamline financial processes, improve transaction tracking, and ensure compliance with evolving regulations, thereby driving the adoption of corporate cards as a vital component of modern financial management strategies.

For instance, in March 2024, Citi and Mastercard introduced commercial card programs in Morocco, representing a key step in expanding their payment solutions within North Africa. The initiative is designed to improve the efficiency of business payments by offering Moroccan enterprises access to modern corporate card services tailored for streamlined financial operations.

Restraint

High Annual Fees and Costs

Corporate cards, particularly premium ones, often come with high annual fees and transaction costs, which can be prohibitive for smaller businesses. These expenses, coupled with transaction fees that escalate with international dealings, pose a significant barrier to adoption.

Smaller businesses, particularly those with limited financial resources, may find it difficult to justify paying for these expenses, which could hinder the adoption of corporate cards. Despite the introduction of corporate cards into their financial systems, many businesses still face difficulties with these money issues.

For instance, in January 2025, HDFC Bank’s corporate credit cards highlight the significant fees and costs associated with commercial cards. The bank’s corporate credit cards come with annual fees, which vary based on the card type and benefits offered. These charges can be a deterrent for smaller businesses, especially those with limited budgets, as they add to the overall cost of managing corporate expenses.

Opportunities

Growth in Emerging Markets

Emerging markets such as India, China, Africa, and Latin America offer strong growth potential for the commercial corporate card market. As digital finance systems improve and the middle class expands, businesses in these regions are upgrading their financial processes. This shift is driving demand for secure, transparent, and efficient expense management tools, positioning corporate cards as essential instruments in fast-growing economies.

For instance, in April 2025, Federal Bank launched a credit card tailored for SME customers in collaboration with NPCI and Visa, marking a significant step in the growth of commercial corporate cards in emerging markets. This new offering aims to provide small and medium-sized enterprises (SMEs) in India with easier access to credit, enabling them to manage their expenses, enhance cash flow, and streamline payment processes.

Challenges

Security Concerns and Fraud Risk

The increasing prevalence of corporate card use has led to a rise in the risk of fraud and cyberattacks. Data theft, unauthorized transactions, and hacking attempts can pose serious threats to businesses. To reduce these risks, companies should invest in better security systems such as encryption and fraud detection tools. Robust security needs increase costs and make systems more complex, creating challenges for secure card usage.

For instance, in May 2025, Marks & Spencer experienced a major cyber attack that disrupted its operations and exposed critical vulnerabilities in digital payment infrastructures. The breach compromised sensitive corporate data and brought attention to the pressing cybersecurity risks associated with modern payment systems, including commercial and virtual corporate cards.

Key Market Segments

By Type

Virtual Cards

Purchasing Cards

Travel and Entertainment Cards

All-in-one Cards

Others

By Card Type

Open-loop Card

Closed-loop Card

By End-User

Small & Medium Enterprises (SMEs)

Large Enterprises

Key Regions and Countries

North America

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Key Players Analysis

Several major financial institutions are playing a significant role in shaping the commercial corporate card market. Companies like American Express Company, JP Morgan Chase & Co., and Citigroup, Inc. are leading the sector with their advanced expense management platforms and corporate solutions. These firms focus on expanding their digital capabilities to support global enterprises.

Key players in the banking sector such as Bank of America Corporation, U.S. Bancorp, HDFC Bank Limited, ICICI Bank Limited, and Kotak Mahindra Bank Limited are also expanding their reach in the commercial card ecosystem. Their focus lies in delivering secure and customizable card programs that meet the needs of domestic and international clients.

Meanwhile, other notable firms such as AirPlus International Ltd., Wex Inc., NGC US, LLC, Bank of China Limited, IndusInd Bank Limited, Citibank, Hong Kong and Shanghai Banking Corporation, and Standard Chartered Bank Limited are actively strengthening their regional and sector-specific offerings. These players are investing in mobility solutions, open-loop card systems, and virtual card infrastructure.

Top Key Players in the Market

AirPlus International Ltd.

Amazon.com, Inc.

American Express Company

Bank of America Corporation

Citigroup, Inc.

JP Morgan Chase & Co. Inc.

U.S. Bancorp

Wex Inc.

NGC US, LLC

Bank of China Limited

HDFC Bank Limited

ICICI Bank Limited

Induslnd Bank Limited

Kotak Mahindra Bank Limited

Citibank

Hong Kong and Shanghai Banking Corporation

Standard Chartered Bank Limited

Other Key Players

Recent Developments

In March 2024, AirPlus International announced a strategic partnership with Billhop to offer businesses more flexible corporate payment options. This collaboration enables companies to make payments via credit card for a broader range of expenses, including those traditionally paid by bank transfer.

In early 2024, Amazon selected American Express to launch a co-branded credit card for U.S. small businesses. This collaboration aims to provide small business owners with enhanced purchasing power and tailored financial solutions, specifically designed to support their operations on Amazon’s platform.

Report Scope