United States Antimony (UAMY) is back in focus after securing a $27 million Department of War contract, a separate $245 million five year sole source agreement, and releasing a large Fostung Tungsten resource estimate.

See our latest analysis for United States Antimony.

The stock’s recent contracts and media exposure have gone hand in hand with sharp momentum. It has a 30 day share price return of 30.43% and a 90 day share price return of 89.70%, while the 1 year total shareholder return is close to 7x. This points to strong interest that may reflect shifting views on growth prospects and risk.

If these moves in United States Antimony are catching your eye, it could be a moment to look at other critical materials names, starting with our 29 best rare earth metal stocks as a curated discovery list.

Yet with UAMY’s shares already up sharply and trading only around 3% below one analyst price target, the key question is whether recent contracts and resources leave upside on the table, or if the market is already pricing in future growth.

Most Popular Narrative: 3% Undervalued

United States Antimony’s most followed narrative pegs fair value at $11.58, slightly above the last close at $11.23, which keeps expectations finely balanced.

US Antimony is expanding its domestic processing capacity (for example, a sixfold increase at the Thompson Falls facility is expected by year end) and increasing ore supply both from its own Montana/Alaska projects and multiple new international sources. This is expected to support higher production volumes and sustained revenue growth through increased throughput and supply security.

Want to see what is backing that fair value call? The narrative leans on steep revenue expansion, a sharp earnings swing, and a future profit multiple that breaks with the company’s past.

Result: Fair Value of $11.58 (ABOUT RIGHT)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, permitting setbacks at Alaska and Ontario projects, along with supply risks around ore quality and external partners, could quickly challenge the upbeat growth narrative.

Find out about the key risks to this United States Antimony narrative.

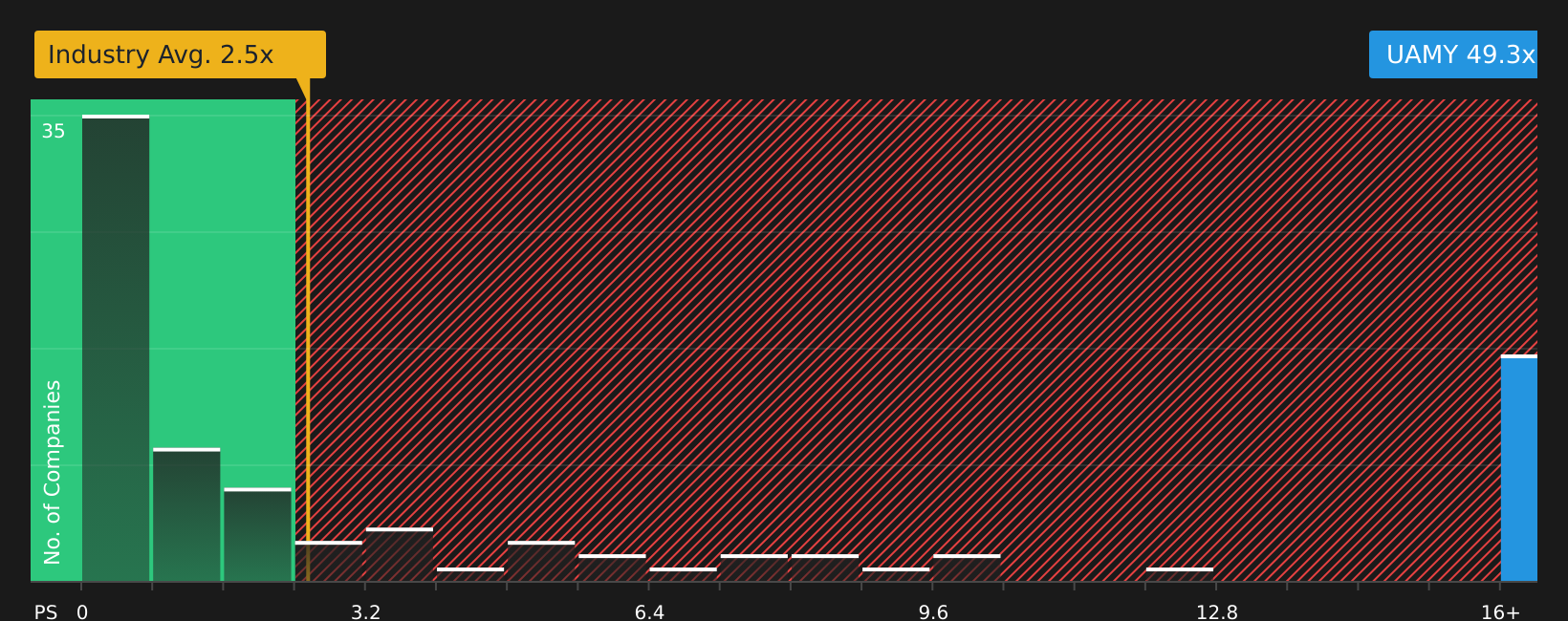

Another Angle On Price

That 3% “about right” fair value view sits next to a very different message from simple sales based pricing. UAMY trades on a P/S of 49.3x, compared with 2.5x for the US Metals and Mining industry, 7.2x for peers, and a fair ratio of 6.6x. With that kind of gap, how comfortable are you with execution risk being priced in so heavily?

See what the numbers say about this price — find out in our valuation breakdown.

NYSEAM:UAMY P/S Ratio as at Mar 2026Next Steps

NYSEAM:UAMY P/S Ratio as at Mar 2026Next Steps

If this mix of optimism and concern feels finely balanced, it may be helpful to act promptly and evaluate the full picture for yourself with 1 key reward and 2 important warning signs.

Looking for more investment ideas?

Do not stop your research with a single stock. Use this moment to broaden your watchlist with ideas that match your goals and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com