United States Antimony (UAMY) has just reported its FY 2025 numbers, with Q4 revenue of about US$13.0 million and a basic EPS loss of roughly US$0.002. Trailing 12 month figures show revenue at around US$39.3 million and a basic EPS loss of about US$0.035. Over the past six reported quarters, revenue has moved from roughly US$2.6 million in Q3 2024 to US$13.0 million in Q4 2025, with quarterly EPS ranging between a profit of about US$0.0048 and a loss of roughly US$0.039. This sets up a picture where topline scale is building but profitability remains under pressure, keeping margins front and center for investors.

See our full analysis for United States Antimony.

With the headline results in place, the next step is to set these numbers against the most widely held stories about United States Antimony to see which narratives hold up and which ones the latest margin profile calls into question.

See what the community is saying about United States Antimony

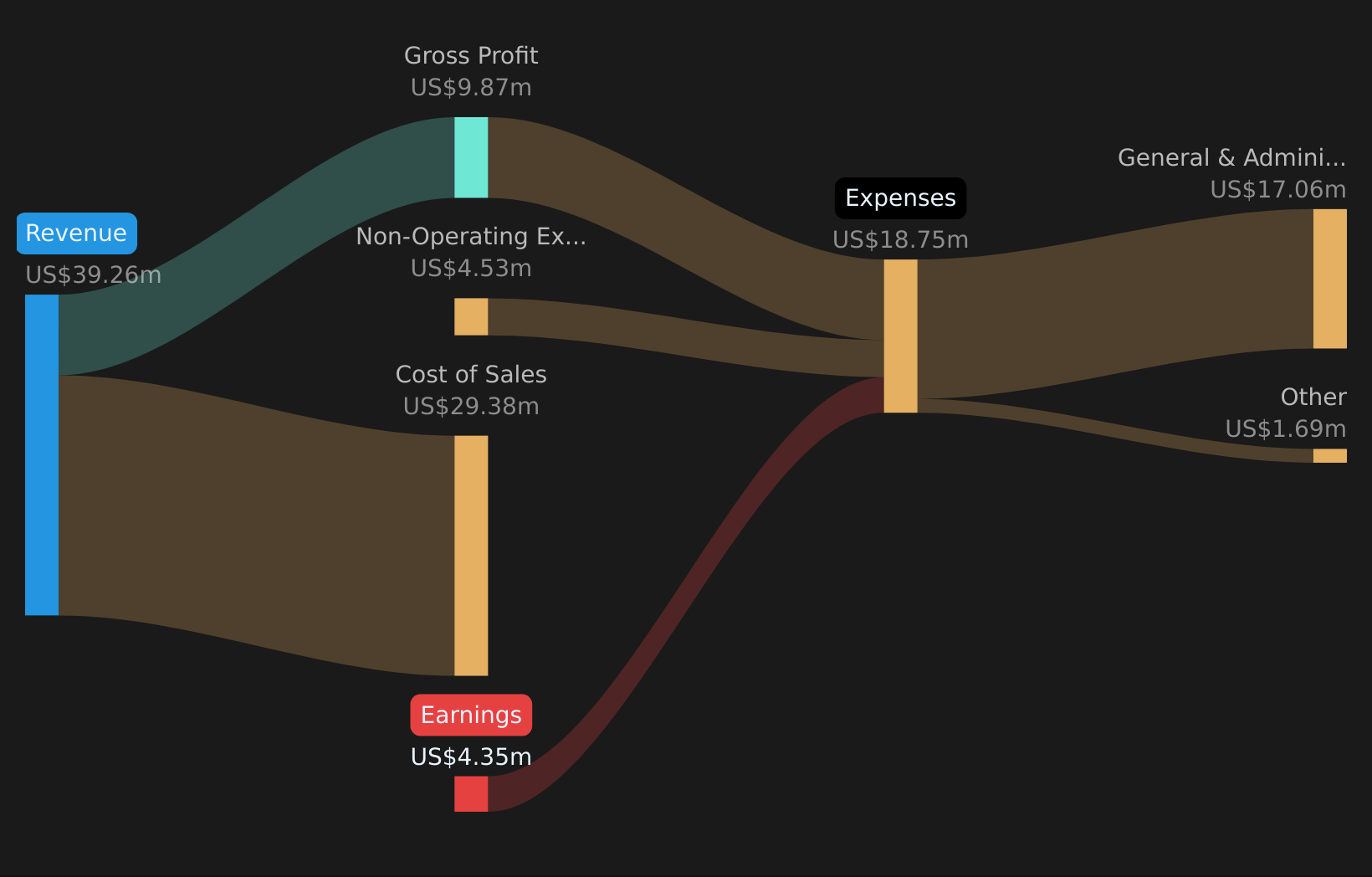

NYSE:UAMY Revenue & Expenses Breakdown as at Mar 2026 Revenue nearly triples year on year, but trailing losses remain Q4 2025 revenue of about US$13.0 million compares with roughly US$5.6 million in Q4 2024, yet trailing 12 month net income is still a loss of around US$4.3 million on about US$39.3 million of revenue. Consensus narrative talks about expanded processing capacity and new ore sources supporting sustained growth, and the reported jump in quarterly revenue alongside a trailing loss of US$4.3 million tests that view as investors weigh higher throughput against the fact that earnings over the last 12 months remain negative.

NYSE:UAMY Revenue & Expenses Breakdown as at Mar 2026 Revenue nearly triples year on year, but trailing losses remain Q4 2025 revenue of about US$13.0 million compares with roughly US$5.6 million in Q4 2024, yet trailing 12 month net income is still a loss of around US$4.3 million on about US$39.3 million of revenue. Consensus narrative talks about expanded processing capacity and new ore sources supporting sustained growth, and the reported jump in quarterly revenue alongside a trailing loss of US$4.3 million tests that view as investors weigh higher throughput against the fact that earnings over the last 12 months remain negative.

On one hand, moving from roughly US$2.6 million of revenue in Q3 2024 to US$13.0 million in Q4 2025 lines up with the idea that more capacity and sourcing are feeding into higher sales. On the other, a trailing EPS loss of about US$0.035 shows that, despite this higher scale, the company has not yet translated that volume into positive net income. EPS swings highlight execution risk for bullish case Within FY 2025, basic EPS moved from a profit of roughly US$0.0048 in Q1 and US$0.0015 in Q2 to losses of about US$0.0388 in Q3 and US$0.0021 in Q4, while trailing EPS over the last 12 months sits at a loss of approximately US$0.035. Bulls point to forecasts of roughly 31.1% annual revenue growth and 35.5% earnings growth, yet the sharp move from positive EPS early in 2025 to a Q3 loss of about US$0.0388 highlights the bearish concern that ramping throughput and contracting for volume can still coincide with losses when pricing or costs move against the company.

The bullish narrative leans on capacity expansions at Thompson Falls and Madero and long term contracts such as the US$245 million Defense Logistics Agency award. The FY 2025 pattern shows that even with these growth drivers in motion, profitability can still swing back into loss territory. Bears also flag permitting, logistics and feedstock quality issues across multiple projects and supply routes. The step from a small Q2 profit of around US$0.18 million to a Q3 loss of roughly US$4.8 million illustrates how operational or market pressures can quickly affect the bottom line. On a quarter like this where revenue is growing but EPS remains choppy, bulls argue future government contracts and higher margin volumes could reshape the story, while critics focus on whether these swings signal deeper earnings risk over time. 🐂 United States Antimony Bull Case Rich P/S multiple meets mixed profitability track record The stock trades on a P/S of about 29.1x against peer and industry averages of roughly 5x and 2.3x, while trailing 12 month net income is a loss of about US$4.3 million and analysts’ blended price target of US$11.58 sits above the current share price of US$8.16. Skeptics highlight that losses have grown at around 23.9% per year over the past five years and that cash runway is under one year. The combination of a high 29.1x P/S multiple with recent shareholder dilution and ongoing losses provides concrete backing for the bearish worry that the current valuation already reflects aggressive expectations for growth and margin improvement.

Analysts are expecting profitability within three years and see upside from US$8.16 toward a target near US$11.58, yet the negative trailing EPS of roughly US$0.035 and a recent quarterly loss of about US$0.29 million in Q4 2025 mean that any path to those outcomes still depends on a meaningful shift in earnings. The short cash runway, coupled with the fact that shares have already been diluted over the past year, feeds the bearish concern that further capital raising could be needed if future cash generation does not keep pace with the current growth and expansion plans. Skeptics point to the rich sales multiple and short cash runway and question whether the current price fully reflects those financing and execution risks. 🐻 United States Antimony Bear Case Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for United States Antimony on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Mixed messages in the data can be useful, because they push you to look closer and decide what really matters for your own plan. To move quickly from headline impressions to a fuller picture of both the concerns and the potential upside, take a look at the 3 key rewards and 3 important warning signs.

See What Else Is Out There

United States Antimony is carrying trailing losses, choppy EPS and a short cash runway along with a rich P/S multiple and recent shareholder dilution.

If those financing and earnings risks feel uncomfortable, shift your attention to companies with stronger financial footing by checking out the solid balance sheet and fundamentals stocks screener (39 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com