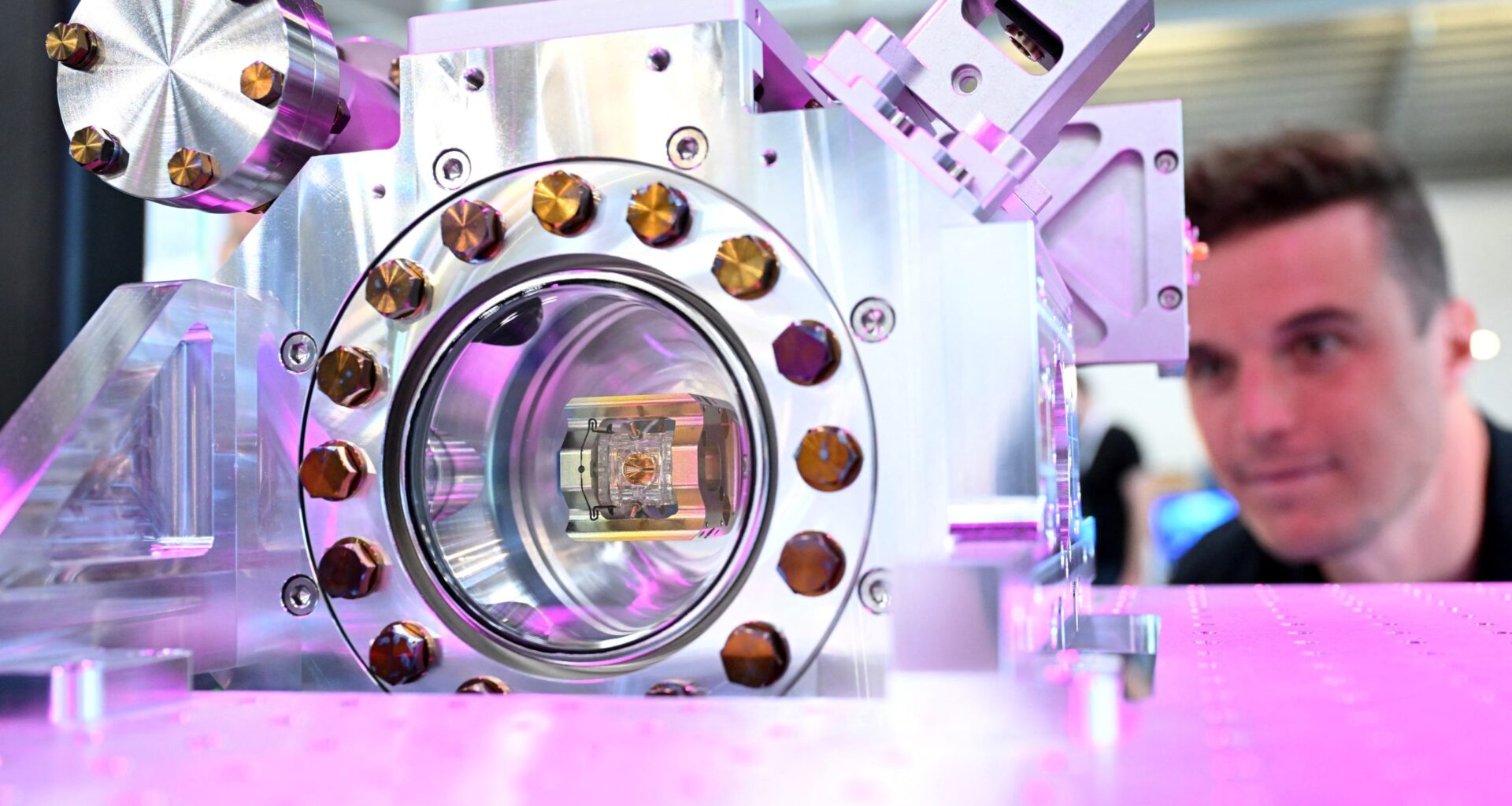

Quantum computing isn’t just faster; it promises a paradigm shift, turbocharging artificial intelligence, upending encryption, and transforming entire industries from drug discovery to logistics, even reshaping defense. While classical computers process information using bits (0s or 1s), quantum computers use qubits – subatomic units that can be 0, 1, or both at once thanks to a principle called superposition. This allows quantum to supercharge computing speeds and multitasking.

Europe has entered the quantum race with a sovereignty-first strategy and billions in public backing – but can it outplay a US ecosystem supercharged by venture capital and commercial clout? While Brussels wants to industrialize quantum on its own terms, with no US cloud giants or Chinese tech pipelines, Washington is racing ahead with private-sector firepower. Beijing, in turn, bets big on state-led muscle.

Globally, the quantum scene is fragmented. The UK jumped in early, launching its National Quantum Programme in 2014, backing four major hubs and startups such as Orca Computing and Universal Quantum. London recently pledged £2.5 billion through the next decade. Canada, Japan, and Israel are betting on hybrid firepower – combining public money, private investment, and academic power. Canada is investing $264 million in over 100 projects nationwide; Japan is directing almost half a billion dollars to centralized R&D hubs in Tsukuba; and Israel’s National Quantum Center unites government, universities, and agile startups.

But the main competition remains between Europe, the US, and China. In quantum, Europe punches above its tech weight. It is home to eight of the nineteen new quantum ventures launched globally in 2024. Hardware frontrunners like IQM Quantum Computers, Alice & Bob, and Pasqal – are now joined by a growing constellation of emerging players, evidence of Europe’s deep scientific roots turning into commercial momentum.

The European Commission recently unveiled a sweeping Quantum Strategy. It advances public funds for six quantum chip pilot factories and rolls out a continent-wide Quantum Skills Academy to help train tomorrow’s workforce.

But will this strong public ambition collide against weak private reality? Europe has committed over €11 billion since 2018 yet attracts just 5% of global private quantum investment, compared to the US with 50%. An EU-private hybrid fund is on the way in 2026 to tackle this private funding shortfall.

The US model wields speed, scale, and getting to market first. Private players such as IBM, Google, Microsoft, IonQ, Rigetti, and D-Wave Quantum have poured hundreds of millions of dollars into hardware, software, and quantum-as-a-service. The policy is ruthlessly agile: startups race ahead, and the Pentagon is ramping up interest on quantum, targeting secure comms, and next-gen cryptography.

The US private sector is rushing forward, announcing breakthrough after breakthrough. Microsoft reported this year that it had built what is known as a “topological qubit,” a new kind of computer chip that combines the strengths of the semiconductors that power classical computers with the superconductors that are typically used to build a quantum computer. Earlier, Google unveiled a quantum computer, based on a computer chip called Willow, that “needed less than five minutes to perform a mathematical calculation that one of the world’s most powerful supercomputers could not complete in 10 septillion years, a length of time that exceeds the age of the known universe.”

Get the Latest

Sign up to receive regular Bandwidth emails and stay informed about CEPA’s work.

It’s not just the large American companies who are making breakthroughs – DWave Quantum, founded in Canada and now publicly listed in the US, recently claimed quantum advantage on a real-world optimization problem, solving it in minutes – compared to a classical system that would have taken millennia. Its breakthroughs in quantum annealing, a special type of quantum computing that helps find the best solution to complex problems, are already being deployed in logistics, manufacturing, and traffic systems, making it one of the few delivering real-world results today.

China is the third giant in the quantum race. Beijing is going big with $15 billion in state-led funding for quantum and a colossal $138 billion government-backed hard-tech venture fund spanning AI, quantum, hydrogen, and more – outspending the rest in its bid for long-term dominance. By comparison, US federal funding to date remains near $6 billion, while the EU has mobilized more than €11 billion in public quantum investment.

Quantum investment is shifting from science to scale. In Q1 2025 alone, $1.25 billion flowed into quantum firms – 70% of last year’s total in just three months. With projections hitting $173 billion by 2040, quantum is no longer just frontier tech, it’s becoming an economic and geopolitical force.

Democratic allies coordinate R&D and standards via the OECD and G7, but export controls and supply chain barriers are rising. The US is clamping down on quantum tech exports to China; Europe enforces export rules on goods, software, and technologies with dual-use civilian and military potential; China drives ahead with state-backed, closed supply chains.

In this fractured battlefield, interoperability and trust are not afterthoughts, they’re the new front in the fight for strategic advantage. Whoever sets the standards and builds the networks doesn’t just shape technology – they command its control. Control over quantum infrastructure means long-term geopolitical leverage, just like the digital dominance US and Chinese tech giants now command.

For Europe, quantum offers a rare chance to reset its industrial destiny, before it’s locked into dependence on the US or China. The race won’t be won with a splash of cash or a one-off policy push. It’ll be decided over the next decade by those who can scale usable systems, shape the rules and standards of trust, and secure the supply chains.

Padraig Nolan is a Non-resident Fellow with the Tech Policy Program at the Center for European Policy Analysis. He serves as Chief Operating Officer of ETPPA, a prominent EU fintech association. He is also an advisory board member of the Lisbon-based Europe Startup Nations Alliance. Padraig holds a bachelor’s degree in law and economics (University of Galway) and a master’s degree in European law (Utrecht University).

Bandwidth is CEPA’s online journal dedicated to advancing transatlantic cooperation on tech policy. All opinions expressed on Bandwidth are those of the author alone and may not represent those of the institutions they represent or the Center for European Policy Analysis. CEPA maintains a strict intellectual independence policy across all its projects and publications.

CEPA Europe’s Tech & Security Conference in Brussels.

Read More From Bandwidth

CEPA’s online journal dedicated to advancing transatlantic cooperation on tech policy.