This buyers’ strike, which started in mid-2022, completes its third year.

By Wolf Richter for WOLF STREET.

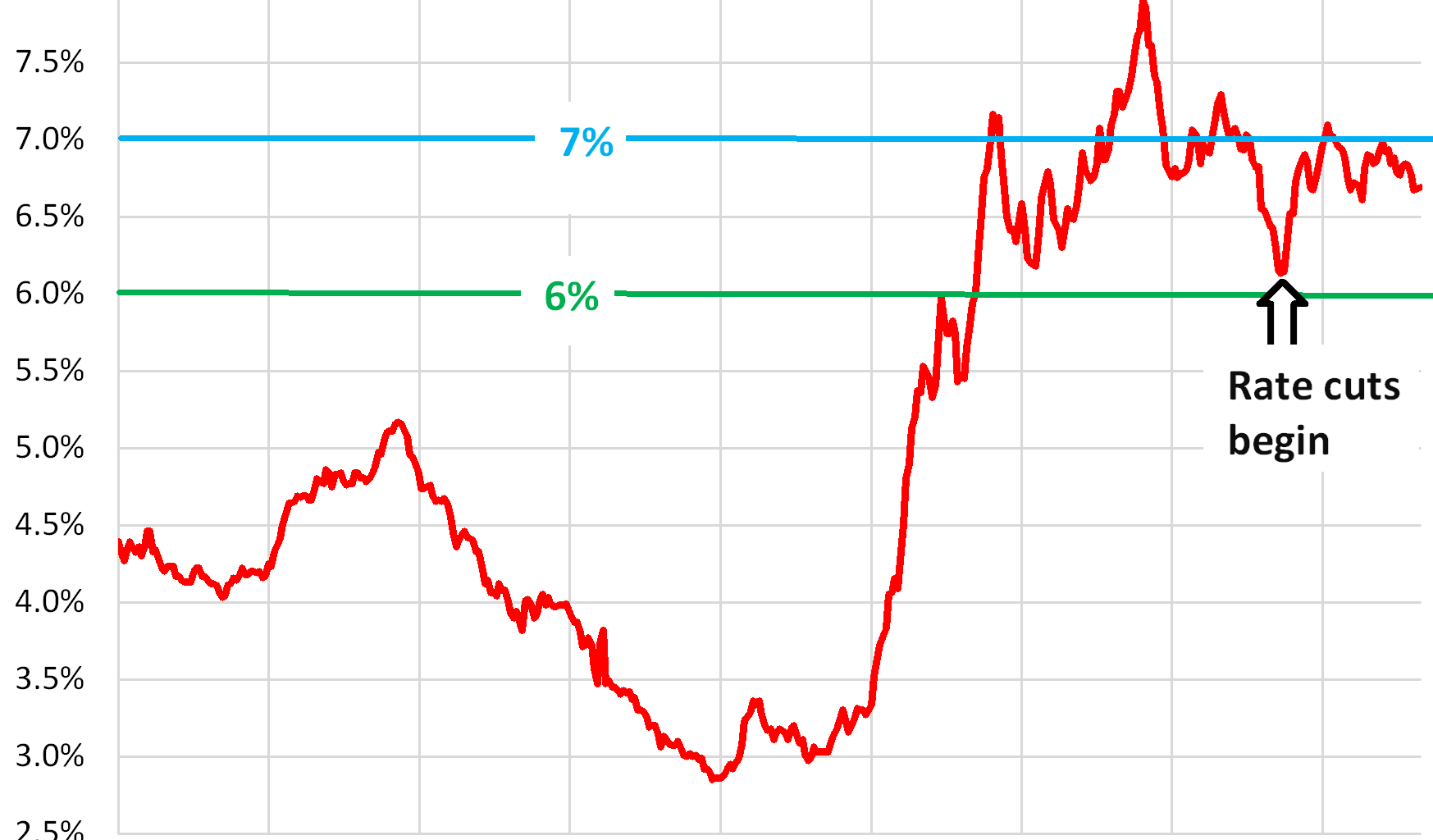

Mortgage rates ticked up a hair for the second week in a row to 6.69%, and have been in this range between 6.6% and 7.1% since October last year, with the average conforming 30-year fixed mortgage rate at 6.69% in the latest week, according to the Mortgage Bankers Association today.

Mortgage rates re-spiked by about 100 basis points from mid-September 2024 into January 2025, following with long-term Treasury yields, while the Fed cut by 100 basis points, despite inflation re-accelerating. This dovish move by the Fed in 2024, in face of accelerating inflation, spooked the long-term bond market, and thereby the mortgage market. The bond market is not to be trifled with.

As this 100-basis-point spike was unfolding, the Fed started talking tough on inflation at the December meeting, indicating that this was its last rate cut for a while. The purpose was to stop long-term yields and mortgage rates from spiking further. The tough talk grew into 2025, and there were no more rate cuts, and it worked in soothing the rattled nerves of the bond market, and mortgage rates stabilized.

But the bond market has remained on edge, leerily watching the Trump administration’s all-out determination to impose its will on the Fed to cut rates by a lot, despite accelerating inflation.

There are two more inflation measures to be released before the Fed’s September meeting. And they’re not going to be pretty. But the Fed, under enormous pressure to knuckle under, may cut anyway, regardless of what inflation does.

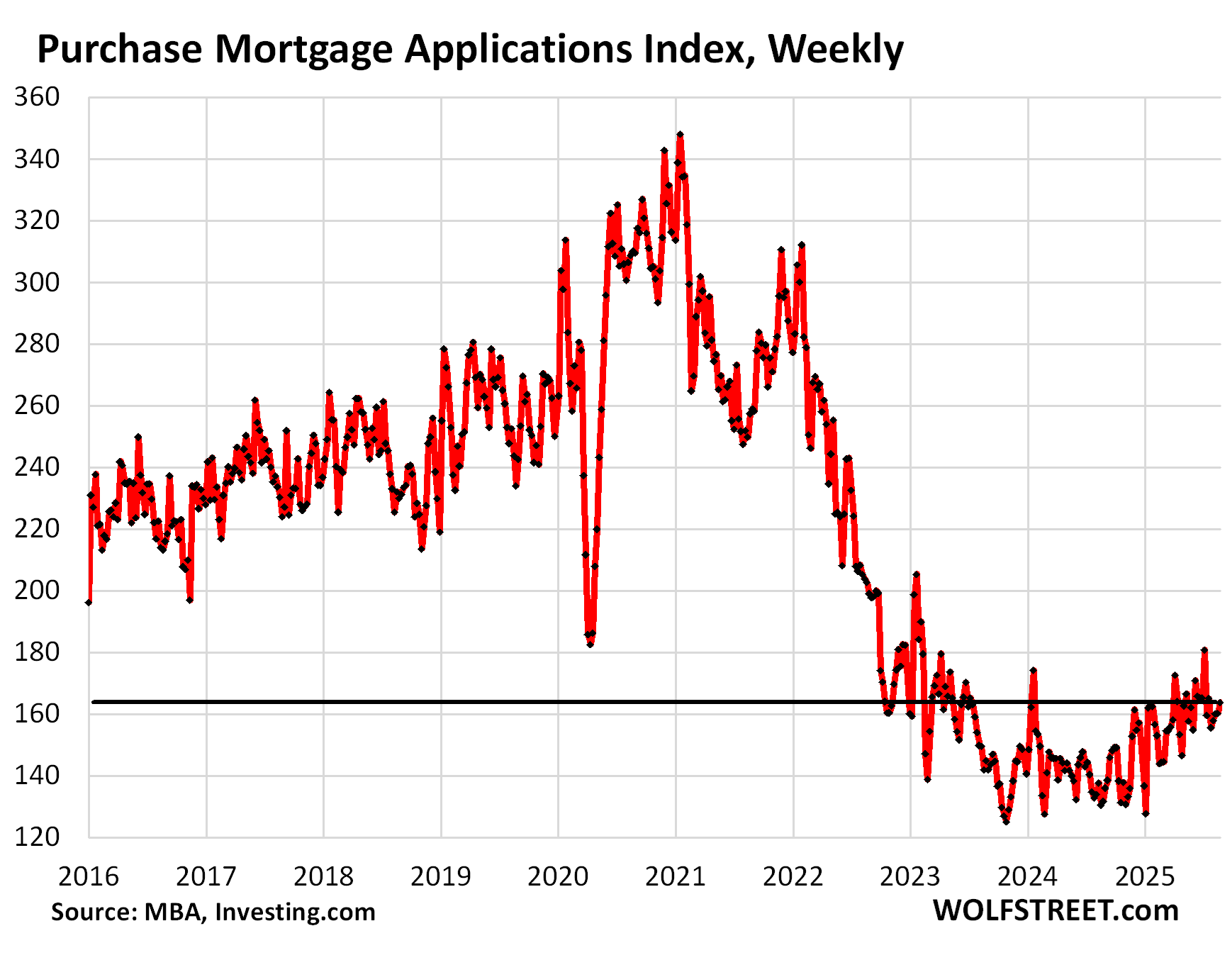

Mortgage demand remains in the deep freeze.

Mortgage applications to purchase a home were still down by 30% from the same week in 2019, and have been in the same range all year. In the latest week, they ticked up a hair, but were lower than they’d been a month ago and two months ago, according to MBA data today.

Mortgage applications have been wobbling along very low levels, showing that demand for mortgages along with demand for homes remain in the deep freeze, after prices exploded between early 2020 and mid-2022.

These too-high prices triggered demand destruction on a historic scale, a fundamental economic principle. And that demand destruction is now showing up in prices in many markets:

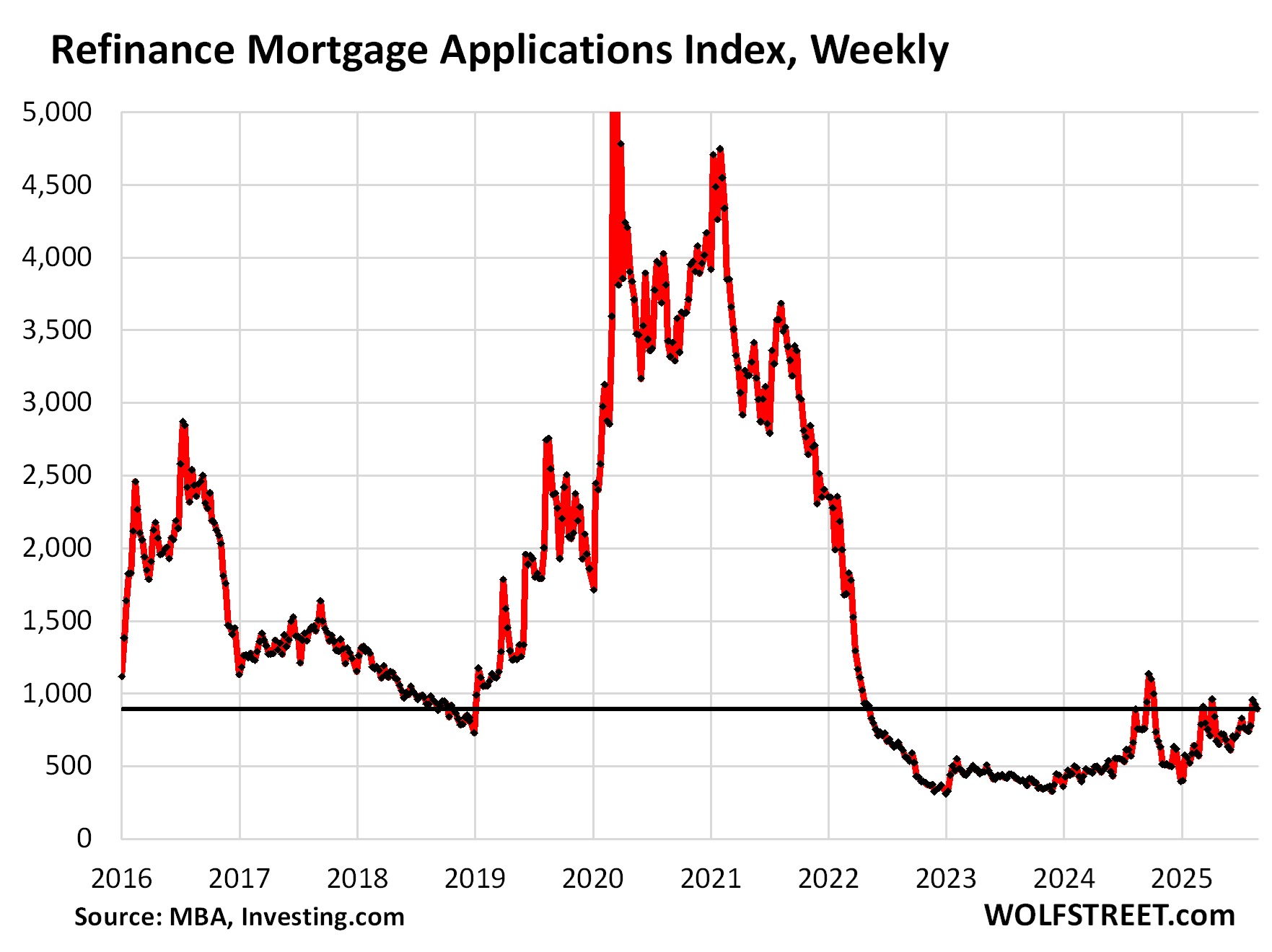

Mortgage applications to refinance a home dipped a hair for the second week and were down by 65% from the same week in 2019. They also have been hobbling along very low levels since early 2022.

But homeowners still want to refinance mortgages for various reasons, and so some refinancings are still happening despite the higher mortgage rates.

Many homebuyers remain on strike.

This buyers’ strike, which started in mid-2022, has now completed its third year. They’re waiting for prices to come down, they’re waiting for their household incomes to rise, and they’re waiting for rates to come down.

Some of them are already homeowners, so they don’t put their homes on the market either.

And others are renters, and in most markets, it’s now far cheaper on a monthly basis to rent a single-family home than to buy an equivalent single-family home – another distortion coming out of the price explosion between early 2020 and mid-2022.

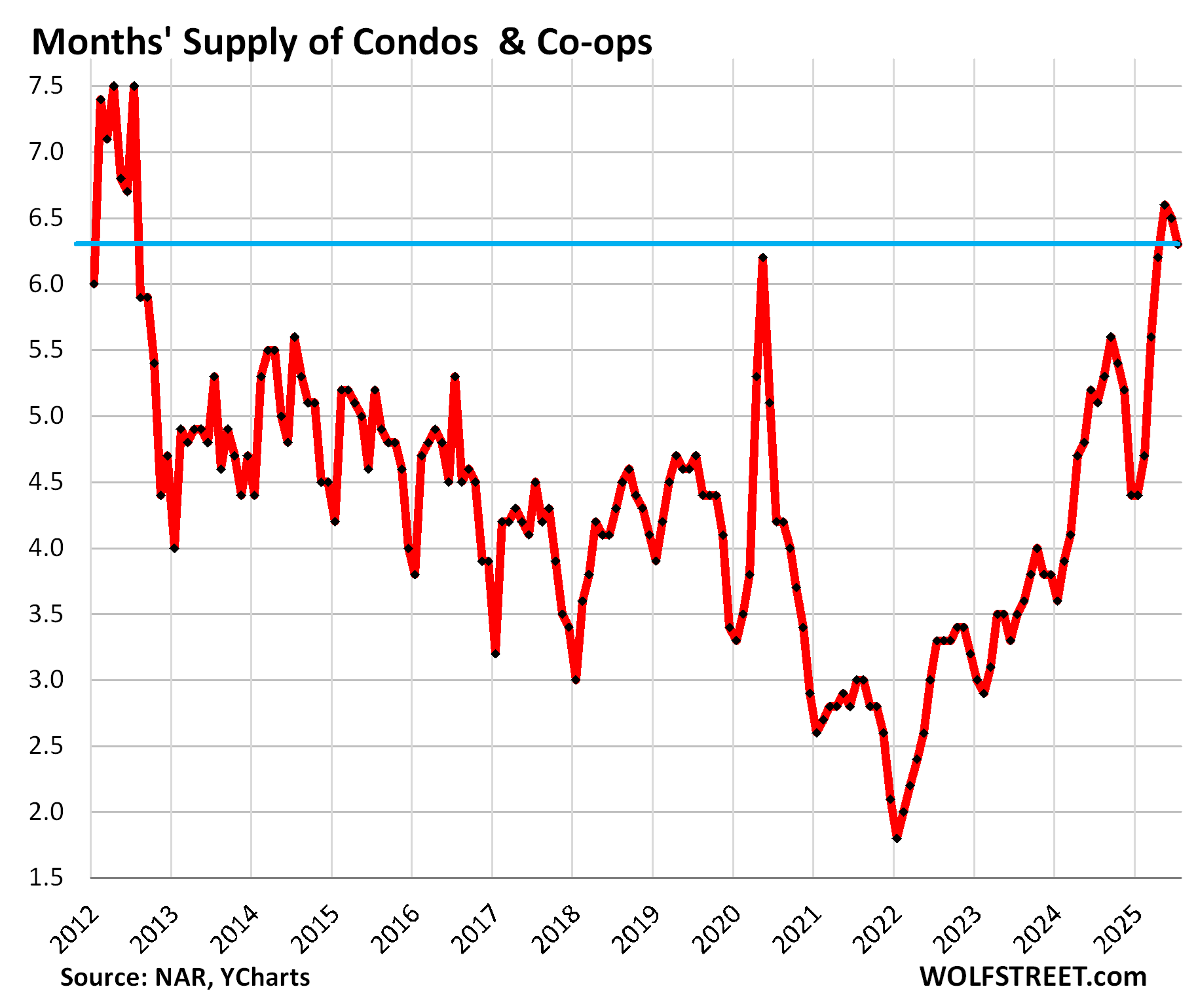

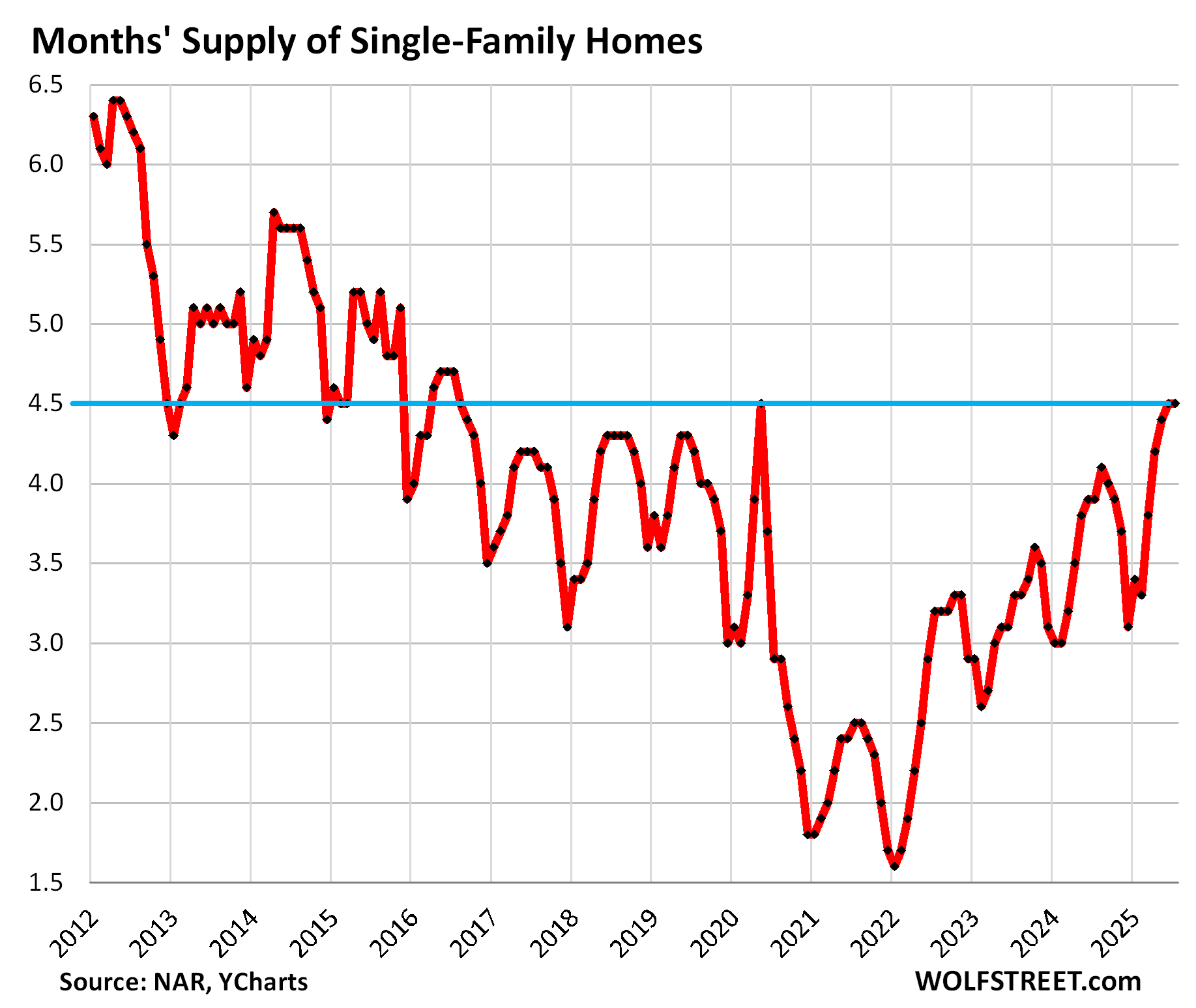

But supply has surged.

Over the past three months, highest supply of condos since the end of the Housing Bust in 2012 (data via National Association of Realtors):

Highest supply of single-family homes since Lockdown May 2020 and before then since mid-2016.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

WOLF STREET FEATURE: Daily Market Insights by Chris Vermeulen, Chief Investment Officer, TheTechnicalTraders.com.