Report Overview

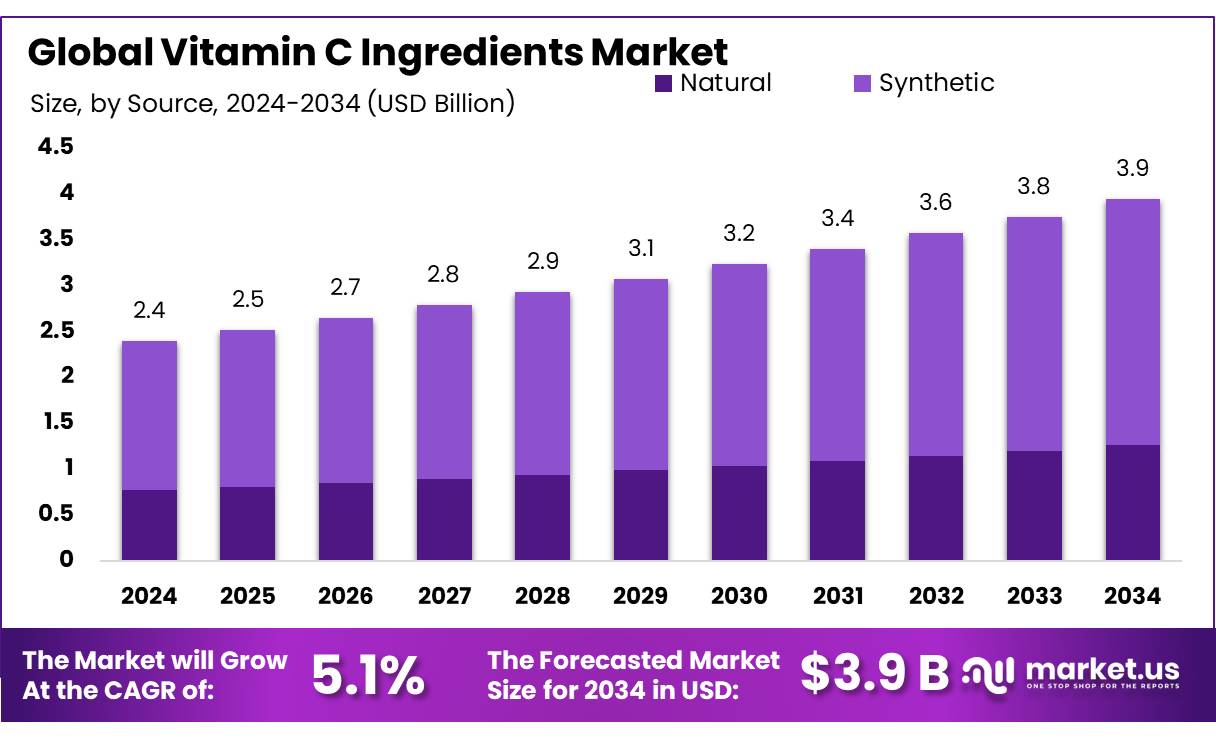

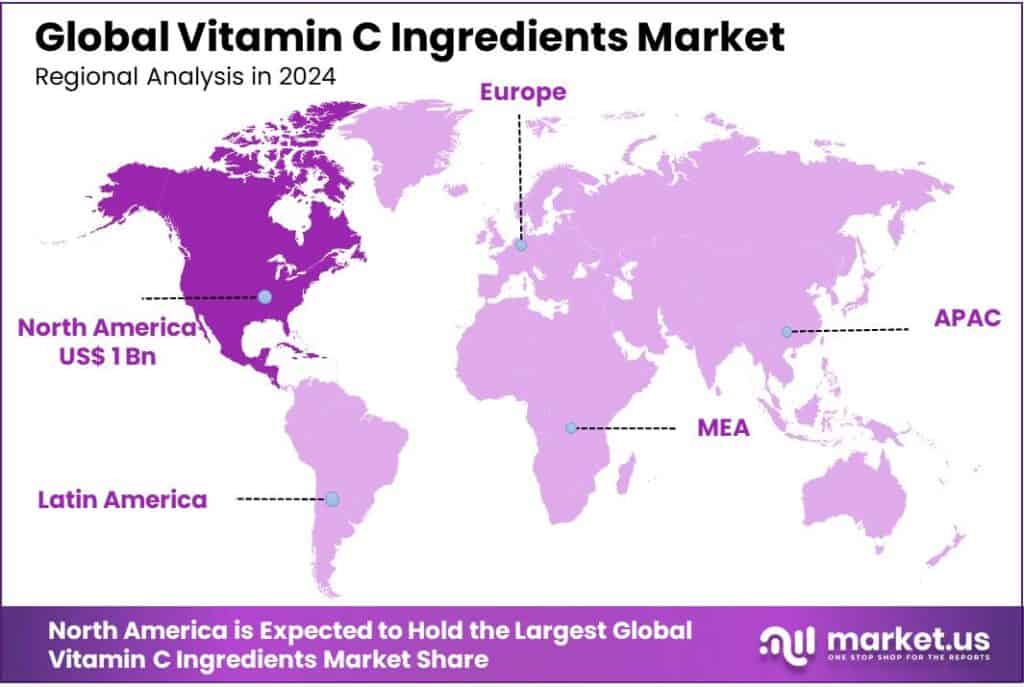

The Global Vitamin C Ingredients Market size is expected to be worth around USD 3.9 Billion by 2034, from USD 2.4 Billion in 2024, growing at a CAGR of 5.1% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 42.7% share, holding USD 1 Billion revenue.

The global vitamin C (ascorbic acid) ingredients industry is a dynamic sector characterized by significant production capacities, robust demand across various applications, and ongoing technological advancements. China remains the dominant player in the global market, accounting for approximately 80% of the world’s vitamin C production.

China stands as the dominant producer, accounting for about 70% of the global supply . In 2022, China’s vitamin C raw material production capacity exceeded 300,000 tons, with exports reaching approximately USD 950 million. The country employs the two-step fermentation process, developed in the 1960s, which involves converting glucose to sorbitol and then to sorbose through fermentation, followed by further fermentation to produce vitamin C.

Government and public health authorities are influencing demand via nutritional policy. In India, the Food Safety and Standards Authority of India (FSSAI) revised the Recommended Dietary Allowance (RDA) for vitamin C, increasing it from 40 mg to 80 mg for men, and from 40 mg to 65 mg for women, effective July 1, 2023.

Vitamin C, or L‑ascorbic acid, remains an indispensable antioxidant ingredient with diverse uses across dietary supplements, food preservation, pharmaceuticals, and cosmetics. Industrially, it is synthesized primarily through the Reichstein process or the modern two‑step fermentation method—both starting from glucose and achieving yields of roughly 60% conversion to vitamin C.

In 2021, global production was estimated at 95,000 metric tons, with China contributing approximately 76,000 metric tons, i.e., around 80% of total supply; the remainder comes from the EU, India, and other regions.

Official government data on pricing indicate that as of 2024, the cost per metric ton of vitamin C ranged from approximately US $2,220 in Shanghai, to US $2,850 in Hamburg, and US $3,490 in the U.S., reflecting regional variations influenced by logistics, regulation, and manufacturing costs

Key Takeaways

Vitamin C Ingredients Market size is expected to be worth around USD 3.9 Billion by 2034, from USD 2.4 Billion in 2024, growing at a CAGR of 5.1%

Synthetic held a dominant market position, capturing more than a 67.9% share in the global vitamin C ingredients market.

Ascorbic Acid Powder held a dominant market position, capturing more than a 31.3% share in the global vitamin C ingredients market.

Dietary Supplements held a dominant market position, capturing more than a 35.5% share in the global vitamin C ingredients market.

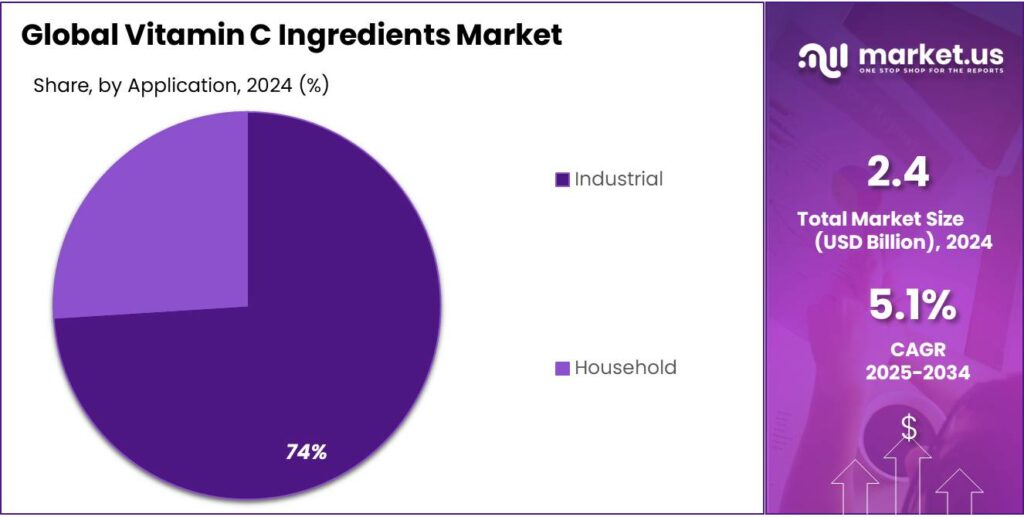

Industrial held a dominant market position, capturing more than a 74.2% share in the global vitamin C ingredients market.

Offline held a dominant market position, capturing more than a 69.7% share in the global vitamin C ingredients market.

North America emerged as a pivotal region in the vitamin C ingredients market, commanding a 42.7% share, which translates to a robust USD 1 billion.

By Source Analysis

Synthetic Vitamin C Dominates with 67.9% Share in 2024 Due to Cost-Effectiveness and Consistent Supply

In 2024, Synthetic held a dominant market position, capturing more than a 67.9% share in the global vitamin C ingredients market. This strong lead is largely driven by the consistent availability, affordability, and scalable production of synthetic vitamin C, which continues to be the preferred choice across food, beverage, pharmaceutical, and cosmetic industries. Unlike natural sources, synthetic vitamin C (ascorbic acid) offers standardized potency, easier formulation compatibility, and extended shelf life, making it ideal for mass production.

Synthetic vitamin C is widely used in multivitamins, energy drinks, fortified snacks, and immune-support supplements. Its popularity is especially evident in countries with large-scale nutritional programs or pharmaceutical manufacturing, where bulk quantities and quality control are essential.

By Form Analysis

Ascorbic Acid Powder Leads with 31.3% Share in 2024 Thanks to Its Versatility and Easy Handling

In 2024, Ascorbic Acid Powder held a dominant market position, capturing more than a 31.3% share in the global vitamin C ingredients market. This segment’s strong presence is due to the powder’s versatility, ease of blending, and long shelf life, which make it highly suitable for use in tablets, capsules, drink mixes, and food fortification. Manufacturers prefer this form for its cost-effectiveness and efficiency in both small-batch and bulk production processes.

Ascorbic acid powder is widely used in dietary supplements and processed foods due to its high purity and water solubility. In 2024, demand surged in health-conscious markets where consumers are increasingly including vitamin C in their daily nutrition to support immunity and energy.

By Application Analysis

Dietary Supplements Lead with 35.5% Share in 2024 as Immunity Support Stays a Daily Priority

In 2024, Dietary Supplements held a dominant market position, capturing more than a 35.5% share in the global vitamin C ingredients market. This growth reflects how vitamin C has become a daily essential for many people focused on immunity, energy, and overall wellness. Whether in chewables, capsules, or effervescent tablets, dietary supplements remain the most common and convenient way for consumers to get a concentrated dose of vitamin C.

Consumer demand for vitamin C supplements remained high, especially in North America and Asia-Pacific, where awareness around preventive healthcare continued to shape buying decisions. The segment also benefited from innovation in delivery forms—like gummies and flavored powders—which made supplements more appealing across age groups.

By End User Analysis

Industrial Users Take the Lead with 74.2% Share in 2024, Driven by Mass Manufacturing Needs

In 2024, Industrial held a dominant market position, capturing more than a 74.2% share in the global vitamin C ingredients market. This overwhelming lead reflects the heavy reliance of large-scale manufacturers on vitamin C as a core ingredient across multiple sectors—including pharmaceuticals, food and beverage, personal care, and animal nutrition. Industries value vitamin C not only for its health benefits but also for its antioxidant properties, which help preserve product quality and shelf life.

The demand from pharmaceutical companies remained especially high in 2024, as vitamin C continued to be widely used in tablets, powders, and immune-support formulations. Similarly, in the food and beverage sector, manufacturers used ascorbic acid as a preservative and nutrient enhancer in juices, snacks, and bakery products. Cosmetic and skincare brands also relied on vitamin C for its role in skin-brightening and anti-aging formulations.

By Distribution Channel Analysis

Offline Channels Lead with 69.7% Share in 2024 Thanks to Easy Access and Consumer Trust

In 2024, Offline held a dominant market position, capturing more than a 69.7% share in the global vitamin C ingredients market. This strong performance was largely due to the widespread availability of vitamin C products through physical retail outlets such as pharmacies, supermarkets, health stores, and wholesale distributors. Consumers often prefer offline channels for immediate access, face-to-face interaction, and the ability to read labels or ask questions before purchase—especially when it comes to health-related products.

In addition to consumer products, offline distribution continues to be the primary channel for bulk vitamin C supply to manufacturers in food, pharmaceuticals, and cosmetics. These B2B transactions are typically handled through long-term vendor relationships, specialized ingredient distributors, or direct sales from ingredient suppliers.

Key Market Segments

By Source

By Form

Crystalline

Ascorbic Acid Powder

Sodium Ascorbate

Calcium Ascorbate

Ester-C

By Application

Food and Beverages

Dietary Supplements

Cosmetics and Personal Care

Pharmaceuticals

Animal Feed

Others

By End User

By Distribution Channel

Emerging Trends

Advancements in Vitamin C Fortification: Embracing Nanotechnology for Enhanced Bioavailability

A notable trend in the vitamin C ingredients industry is the integration of nanotechnology to improve the stability and bioavailability of vitamin C in food products. Traditional fortification methods often face challenges due to the inherent instability of vitamin C, which can degrade when exposed to heat, light, and oxygen. This degradation leads to reduced efficacy and limits the nutritional benefits of fortified foods.

Recent research has focused on developing innovative encapsulation techniques using nanomaterials to protect vitamin C from environmental factors. For instance, studies have explored the use of chitosan-based nanoparticles to encapsulate vitamin C, enhancing its stability and controlled release in the gastrointestinal tract. These advancements aim to ensure that the vitamin remains active and bioavailable, thereby maximizing its health benefits for consumers.

The World Health Organization (WHO) recognizes food fortification as a cost-effective strategy to address micronutrient deficiencies globally. However, the success of such programs depends on the stability and bioavailability of the added nutrients. By adopting nanotechnology-based delivery systems, the industry can overcome the limitations of traditional fortification methods, leading to more effective public health interventions.

Drivers

Government Initiatives and Public Health Strategies

Governments worldwide are increasingly recognizing the importance of vitamin C fortification as a strategic approach to combat micronutrient deficiencies. The World Health Organization (WHO) has highlighted food fortification as one of the most cost-effective public health interventions to address nutrient deficiencies. As of 2020, 143 countries had adopted mandatory food fortification policies, underscoring the global commitment to enhancing public health through improved nutrition.

In India, the Food Safety and Standards Authority (FSSAI) has developed specifications for fortified rice, incorporating essential nutrients like vitamin C. This initiative is part of the government’s broader efforts to integrate fortified foods into public distribution systems, such as the Mid-day Meal Scheme (MDM), Integrated Child Development Scheme (ICDS), and Public Distribution System (PDS). These programs aim to reach vulnerable populations, ensuring they receive adequate nutrition, including vitamin C, to prevent deficiencies.

Internationally, organizations like the World Food Programme (WFP) have implemented vitamin C fortification in food aid commodities. For instance, the U.S. Agency for International Development (USAID) has supported the fortification of blended foods with vitamin C to prevent scurvy among refugee populations. Studies have shown that providing vitamin C through fortified foods can be an effective strategy to address deficiencies in emergency settings.

These government-led initiatives reflect a growing recognition of the critical role vitamin C plays in maintaining public health. By integrating vitamin C into food fortification programs, governments aim to reduce the prevalence of deficiency-related diseases and promote overall well-being among their populations.

Restraints

Challenges in Cost-Effective Vitamin C Fortification

While vitamin C fortification is widely recognized as a cost-effective strategy to combat micronutrient deficiencies, its implementation faces significant challenges, particularly concerning cost-effectiveness and practical considerations.

A comprehensive cost-effectiveness analysis conducted by the Institute of Medicine in 1997 evaluated the impact of increasing vitamin C fortification in U.S.-supplied blended foods, such as Corn-Soy Blend (CSB) and Wheat-Soy Blend (WSB), intended for food aid programs. The study found that enhancing vitamin C levels to 90 mg per 100 g of these blends would cost an additional $6.33 per metric ton.

However, this increase would only benefit a small proportion of the target population, as scurvy and vitamin C deficiency were rare in most recipient groups. Consequently, approximately 93% of the expenditure would be unnecessary, rendering the intervention highly cost-ineffective. The analysis suggested that alternative strategies, such as increasing the overall food ration or improving iron content, would be more effective and efficient in addressing the nutritional needs of the population.

Furthermore, the stability of vitamin C during storage and preparation poses another challenge. Vitamin C is highly sensitive to heat, light, and oxygen, leading to significant losses during the cooking process. In emergency settings, where food aid is often the sole source of nutrition, these losses can undermine the effectiveness of fortification efforts. The variability in vitamin C content due to manufacturing inconsistencies further complicates the situation, as some products may not meet the desired fortification levels.

Opportunity

Government-Led Fortification Initiatives: A Pathway to Enhanced Public Health

One of the most promising avenues for the growth of vitamin C ingredients lies in the Indian government’s robust fortification programs aimed at combating micronutrient deficiencies. These initiatives are not only addressing public health concerns but also creating a conducive environment for the growth of the vitamin C ingredients market.

The Food Safety and Standards Authority of India (FSSAI) has been at the forefront of promoting food fortification. The “Fortification of Food with Micronutrients” regulations, established in 2018, set standards for fortifying staple foods like rice, wheat flour, salt, and edible oil with essential nutrients, including vitamin C. These regulations aim to ensure that fortified foods meet specific nutrient levels, thereby enhancing their nutritional value and contributing to the prevention of deficiencies.

In 2024, the Indian government launched the “Fortified Rice Initiative” to distribute fortified rice enriched with micronutrients such as iron, folic acid, and vitamin B12 to vulnerable populations. While vitamin C is not explicitly mentioned in this initiative, the emphasis on micronutrient enrichment underscores the government’s commitment to improving nutritional standards. The initiative is expected to have a significant impact on public health by addressing deficiencies in essential nutrients.

These government-led fortification programs are creating a favorable market environment for vitamin C ingredients. As the demand for fortified foods increases, manufacturers are seeking high-quality vitamin C ingredients to meet regulatory standards and consumer expectations. This trend presents growth opportunities for suppliers of vitamin C ingredients, particularly those who can provide stable, bioavailable forms of the vitamin that can withstand the processing conditions of food fortification.

Regional Insights

North America Leads with 42.7% Share Worth USD 1 Billion in 2024

In 2024, North America emerged as a pivotal region in the vitamin C ingredients market, commanding a 42.7% share, which translates to a robust USD 1 billion in market value. This strong performance reflects the region’s advanced health infrastructure, rising consumer demand for immunity-support nutrients, and significant adoption of fortified foods, supplements, and pharmaceuticals. North American manufacturers continue to leverage high-quality synthetic ascorbic acid and its variants to power daily wellness routines and product innovation.

The U.S., in particular, remains a central driver—owing to its mature distribution channels, strong e-commerce presence, and growing focus on preventative healthcare. From fortified beverage launches to vitamin-enriched skincare and OTC supplements, vitamin C ingredients are deeply woven into both functional and lifestyle products. Additionally, regulatory clarity on ingredient safety and labeling provides confidence to both brands and consumers, helping to maintain steady demand and price stability.

Key Regions and Countries Insights

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Players Analysis

DSM is a global leader in nutritional ingredients, offering a wide range of vitamin C solutions including pure ascorbic acid, sodium ascorbate, and advanced delivery systems. In 2024, DSM Nutrition generated over €2.3 billion in sales from health and nutrition segments. Their vitamin C ingredients are used in supplements, beverages, and fortified foods. Known for high purity, sustainability, and research-backed formulations, DSM remains a trusted supplier for both consumer and industrial health product manufacturers globally.

Mason Vitamins is a well-established U.S.-based supplement brand offering over 450 products, including a wide variety of vitamin C formats like chewables, capsules, and time-release tablets. In 2024, the company focused on expanding its retail footprint across major pharmacies and online platforms in North America. Their vitamin C offerings target immune health and antioxidant support, with doses ranging from 250 mg to 1000 mg, making them accessible and affordable to a broad consumer base.

NOW Foods continues to be a leading natural products brand in the U.S., offering a broad line of vitamin C options including ascorbic acid powder, chewables, and sustained-release tablets. In 2024, NOW reported estimated revenues of USD 360 million, supporting a wide distribution network including health stores, pharmacies, and e-commerce. Known for affordability, transparency, and clean-label focus, NOW’s vitamin C products are popular among health-conscious consumers looking for daily immune and antioxidant support.

Top Key Players Outlook

DSM

Mason Vitamins

Sabinsa

Now Foods

Roquette

Nature’s Way

Lonza

Jarrow Formulas

BulkSupplements

Ashland

Recent Industry Developments

Nature’s Way, headquartered in Green Bay, Wisconsin, is recognized for its extensive range of herbal supplements and vitamins, including vitamin C products. As of August 2025, the company reported annual revenues of around USD 750 million and employed approximately 831 individuals across five continents.

In 2024 DSM-Firmenich, reported that its vitamin transformation program contributed approximately €100 million to its Adjusted EBITDA, reflecting its strategic focus on enhancing its vitamin portfolio.

Report Scope