Economists have long understood that demographic changes would result in slower growth in the labor supply as baby boomers retire.

But when those changes are combined with a meaningful shift in immigration policy, the result is a decline in labor force participation.

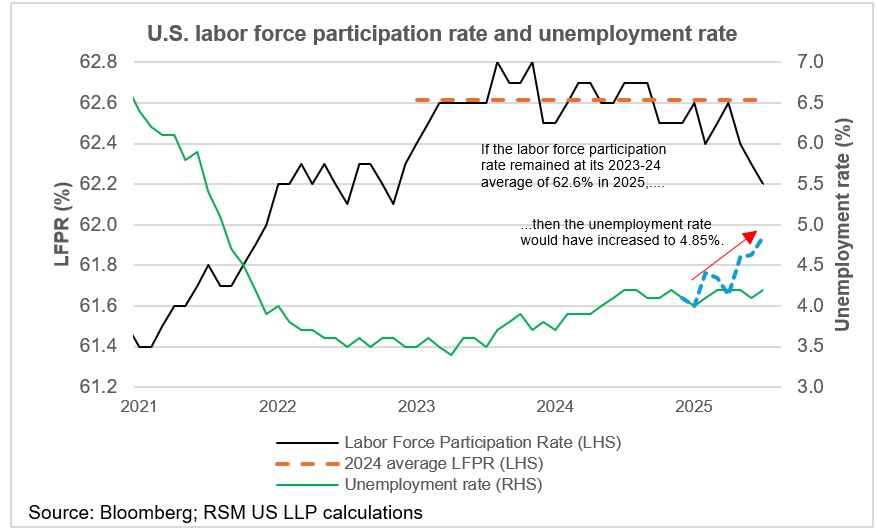

That decline is partially masking the softness in the labor market as the unemployment rate sits at 4.24% even as the breakeven level of jobs needed to keep employment conditions stable has declined to about 50,000.

To examine this, we conducted a simple exercise in which we held the labor force participation rate at its 2023-24 average to estimate what the current unemployment rate would be otherwise.

If the labor force participation rate had held at its 2023-24 average of 62.6% and all else remained the same, the unemployment rate would be sitting near 4.85% compared with the current 4.24%.

This dynamic suggests that the path is open for the Federal Reserve to adopt a risk management stance with respect to the labor market and growth through a 25 basis-point rate cut at its meeting on Sept. 17.

Get Joe Brusuelas’s Market Minute economic commentary every morning. Subscribe now.

Such a reduction, however, would most likely not alter the growing suspicion among investors that the Fed is now prepared to tolerate inflation closer to 3% compared with the official 2% target.

That view is part of an evolving market narrative where the U.S. Treasury curve falls at the short end and rises at the long end. The 2-year has fallen by 76 basis points from its peak on Jan. 13, while the 30-year has increased by 48 basis points since its recent low on April 4.

Given that inflation is likely to continue rising points to the possibility that, with a rate cut, longer-term rates along the curve from 5 years to 30 years may increase as they did following the Fed’s rate reductions last September.