SR

McDermott Will & Schulte

More

![]()

As we look to 2026, exits aren’t just about timing. Dealmakers are utilizing process, planning, and creativity to find new paths to liquidity.

United States

Food, Drugs, Healthcare, Life Sciences

To print this article, all you need is to be registered or login on Mondaq.com.

As we look to 2026, exits aren’t just about timing.

Dealmakers are utilizing process, planning, and creativity to find

new paths to liquidity. Investors across healthcare sectors are

looking to dynamic opportunities while integrating flexible exit

pathways and regulatory readiness to maximize values.

At McDermott Will & Schulte’s HPE NYC 2025 conference,

industry leaders explored new sectors alongside investors’

shifting focus to innovative and deliberate exits. Here, we

continue the conference conversations with a review of emerging

opportunities and strategic exits amid regulatory developments.

In Depth

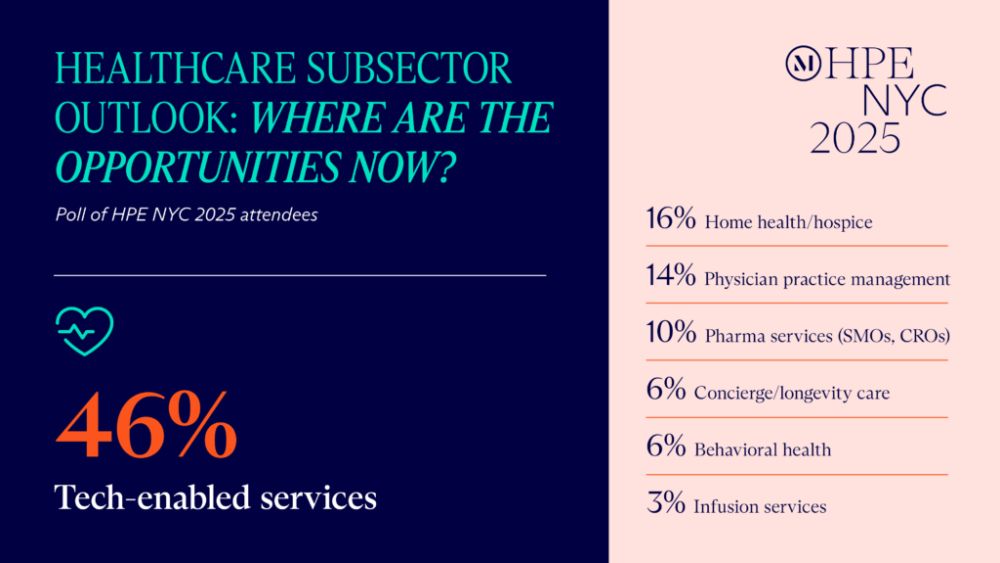

Emerging opportunities

Development and commercialization

partnerships. Strategic acquirers are increasingly

targeting tech-enabled contract research organizations and

commercialization platforms as initial public offerings (IPOs) and

cross-border activity lag. To illustrate, our event panelists noted

investments in drug manufacturing, supply chains, and drug

administration (including pharmacies and infusion centers).

Liquidity is consolidating around those strategic acquirers, which

are historically slower to get to closing and do not pay a private

equity premium.

Pharmaceutical industry. HPE NYC panelists

expect increased mergers and acquisitions activity in the

pharmaceutical industry. Specifically, looming patent cliffs and

the resulting need to replace lost revenue make late-stage,

de-risked assets strong targets with strategic advantages.

Additionally, the panelists pointed to potential for partnerships

in artificial intelligence (AI) and other technologies, which would

enable the development of increasingly comprehensive data

collection and maintenance via life sciences services.

Behavioral health. Demand and competition

continued to grow in the behavioral health sector, with valuation

rates tracking the realities of contract structures, operational

stability, and reimbursements. Notably, the increasing role of

technology is helping enhance success rates and implement

evidence-based care while boosting efficiency in the sector.

Investor-payor collaboration. Our panelists

pointed to the desirability of pursuing potential partnerships to

mitigate current pressures facing physician groups. Collaboration

with payors would help reduce reimbursement lags and offer

opportunities to launch lab services.

Creative exits

Flexible pathways. Private equity is turning

to continuation vehicles and sponsor-to-sponsor trades for flexible

exit pathways, maximizing value as the market’s appetite for

IPOs is diminished.

Trial execution. Platforms that enhance trial

execution, including in the oncology and central nervous system

spheres, offer another framework for creating exits. HPE NYC

panelists pointed out that, given the financial risks in the trial

arena, venture capital investment is common.

Physician practice management (PPM). The

panelists further highlighted the stability and potential for tech

enablement in the PPM sector, predicting an uptick in exits over

the next few years. PPM organizations are less impacted by the

macro dynamics and regulatory issues affecting other industry

businesses, and the improvements driven by technology should

solidify exit opportunities.

Regulatory readiness

Investors face growing risks from fragmented state privacy laws,

HIPAA and Federal Trade Commission enforcement, and US Food and

Drug Administration scrutiny of AI. In fact, 50% of HPE NYC 2025

attendees believe that navigating complex regulatory and compliance

landscapes is the most significant nonfinancial challenge faced by

private equity firms investing in healthcare. Federal and state

regulators are imposing new notice and approval requirements that

have significant transaction implications for healthcare providers,

industry operators, dealmakers, and investors.

Baby HSR. Modeled on the federal

Hart-Scott-Rodino (HSR) Act, “Baby HSR” or

“mini-HSR” laws are state laws that impose notice and

approval requirements on parties to certain healthcare

transactions. While the timing and details vary by state, event

panelists noted concern that these relatively new regulations will

delay deals. As an initial matter, parties should monitor Baby HSR

laws in the states in which they operate (or plan to operate) and

consider the impact that doing business in a state may have on the

timing of future exit transactions.

Work with lawmakers. When new laws are

proposed, it may be wise to turn to lobbyists or public relations

firms in an effort to minimize current deal disruptions or future

exit delays. Building relationships with lawmakers is key, as is

communicating the positive results healthcare investors have

achieved – and continue to achieve – in their

communities.

Readiness audits. A review of the relevant

state’s filing requirements is essential before going to

market. Readiness audits completed in conjunction with regulatory

preparedness help effectively position assets in both strategic and

sponsor exits. In addition to managing the deal timeline, that

analysis may provide alternative structures to minimize filing

requirements.

Conclusion

Looking toward increased activity in dynamic sectors and

creative exit opportunities, stakeholders should consider the

impact of regulatory reforms across the healthcare industry.

As always, we look forward to continuing the conversation with

our clients and partners. To explore these topics further, please

reach out to a member of the firm’s Health & Life Sciences Practice Group.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.