MGO CPA LLP are most popular:

within Real Estate and Construction and Law Practice Management topic(s)

with readers working within the Accounting & Consultancy industries

Key Takeaways:

VPNs can make remote employees appear to be working in another

state and complicate income sourcing and apportionment.

Cost-of-performance states source income where the work is

physically performed, not necessarily where the company’s

headquarters, customers, or servers are located.

Misaligned data can expose organizations and employees to

unexpected multistate tax filing and withholding obligations.

Virtual private networks (VPNs) have become the quiet backbone

of remote work. They keep data secure and employees connected, no

matter where they log in. But there’s a hidden side effect that

few companies consider: when a VPN makes it appear as though an

employee in Texas is working from a server in California, the data

trail can mislead tax systems, auditors, and even internal finance

teams.

With each state applying unique sourcing rules, and budget

shortfalls prompting closer scrutiny, that digital illusion can

translate into very real tax exposure.

The Sourcing Framework

One of the obligations for companies providing services is

determining the correct state in which those services are sourced

for income tax purposes (and possibly sales and payroll tax

purposes). In this context:

Sourcing means the method a state uses to

assign a portion of a company’s receipts (especially from

services or intangibles) to that state.

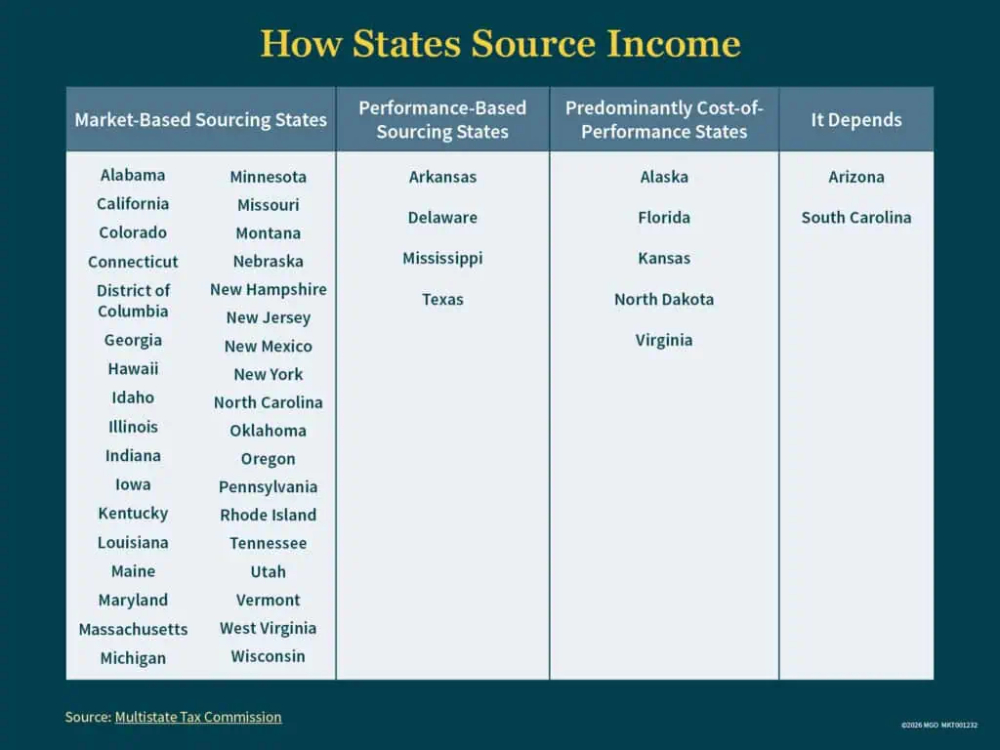

There are two primary methods for sourcing income:

In cost-of-performance (COP) states, receipts

are attributed to where the “income-producing activity”

is performed.

In market-based sourcing (MBS) states,

receipts are attributed to the state where the customer receives

the service benefit or where the intangible is used.

Most states now use market-based sourcing. However, a handful of

states use cost-of-performance rules or mix them with market-based

regulations.

Remote Work + VPN = Sourcing Risk

Now, layer remote working arrangements, VPNs, and multistate

operations onto that patchwork of sourcing rules across states.

A VPN essentially acts as a tunnel between an employee and a

server location. So, for example, the system may show the employee

working in California based on an IP address or VPN endpoint, even

though the employee is working from their home in Texas or a

client’s office in North Dakota.

If the company reports time or allocates revenue based on the

VPN location rather than tracking the employee’s actual

physical work location, the sourcing basis may be incorrectly

skewed.

With a cost-of-performance sourcing state, the place where the

work is performed is critical. If the employee is physically in

Texas but the VPN makes it appear that the work was performed in

California, the company may misassign where the income-producing

activity occurred.

When employees travel or work in multiple states, tracking their

location can be complex. Without accurate records, such as

timesheets with locations, travel logs, and other documents, the

company and its employees may face unexpected multistate filing

obligations.

One Employee, Three States, and a Surprising Tax Bill

Here’s an example of how tax obligations can catch employees

off guard. Say ABC Company is based in California and hires a

remote employee living in Texas and regularly traveling to

corporate locations in Oklahoma and Kansas for work.

The employee may assume that because their home state of Texas

has no individual income tax, they don’t have to file any state

income tax returns. However, Oklahoma requires workers to file

non-resident income tax returns if they earn $1,000 or more in the

state and requires employers to start withholding state income tax

if employees earn more than $300 in any quarter. Kansas requires

workers to file non-resident income tax returns and their employers

to withhold income taxes if the employee spends one day

working in the state.

Since the company has corporate locations in Oklahoma and

Kansas, it presumably is aware of its income, sales, and payroll

tax obligations in those states. But the employee could be caught

off guard at tax time when they realize they need to file

non-resident returns in two states.

Income-Sourcing Issues to Address

Consider the following three steps to protect your organization

and its employees:

1. Track Actual Work Locations

If an employee is physically working at a location other than

your premises, you should have a process to capture that location,

even if they’re using a VPN. For example, maintain timesheets

that specify the state, travel logs for employees working in other

states, and periodically confirm the employee’s state of

residence. These records help support audit positions and align

apportionment with where the work is performed rather than the

virtual network location.

2. Communicate With Employees

Employees should understand that if they work in another state

due to travel or relocation, they may trigger individual income tax

or withholding obligations in that state. Communicate with them

clearly so they’re not surprised by multistate filings or

withholding changes.

3. Establish Internal Controls for Sourcing

Revenue

Consider how you track where services are performed for sourcing

purposes. Don’t rely solely on VPN logs or billing addresses.

Make sure you have a process for reconciling the employee’s

actual location.

Budget shortfalls are forcing many states to pursue audits

around remote work and income sourcing, so ignoring the issue and

hoping you won’t get audited isn’t a sound strategy.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.