Executives from India’s second generation of high-growth startups, built between 2014 and 2025, have spawned a new wave of founders who have created more than 200 firms in the past decade.

Following their stints as executives at 111 companies, 184 founders have launched about 203 startups, highlighting the growing influence of so-called ‘startup mafia’ networks, according to data analysed by Longhouse exclusively for ET.

The term startup mafia refers to cohorts of former employees who go on to build new companies.

The current lot would be the third generation mafia, with the first being the likes of Flipkart and Paytm, and the second being Oyo, Ola and Udaan.

ETtech

ETtech

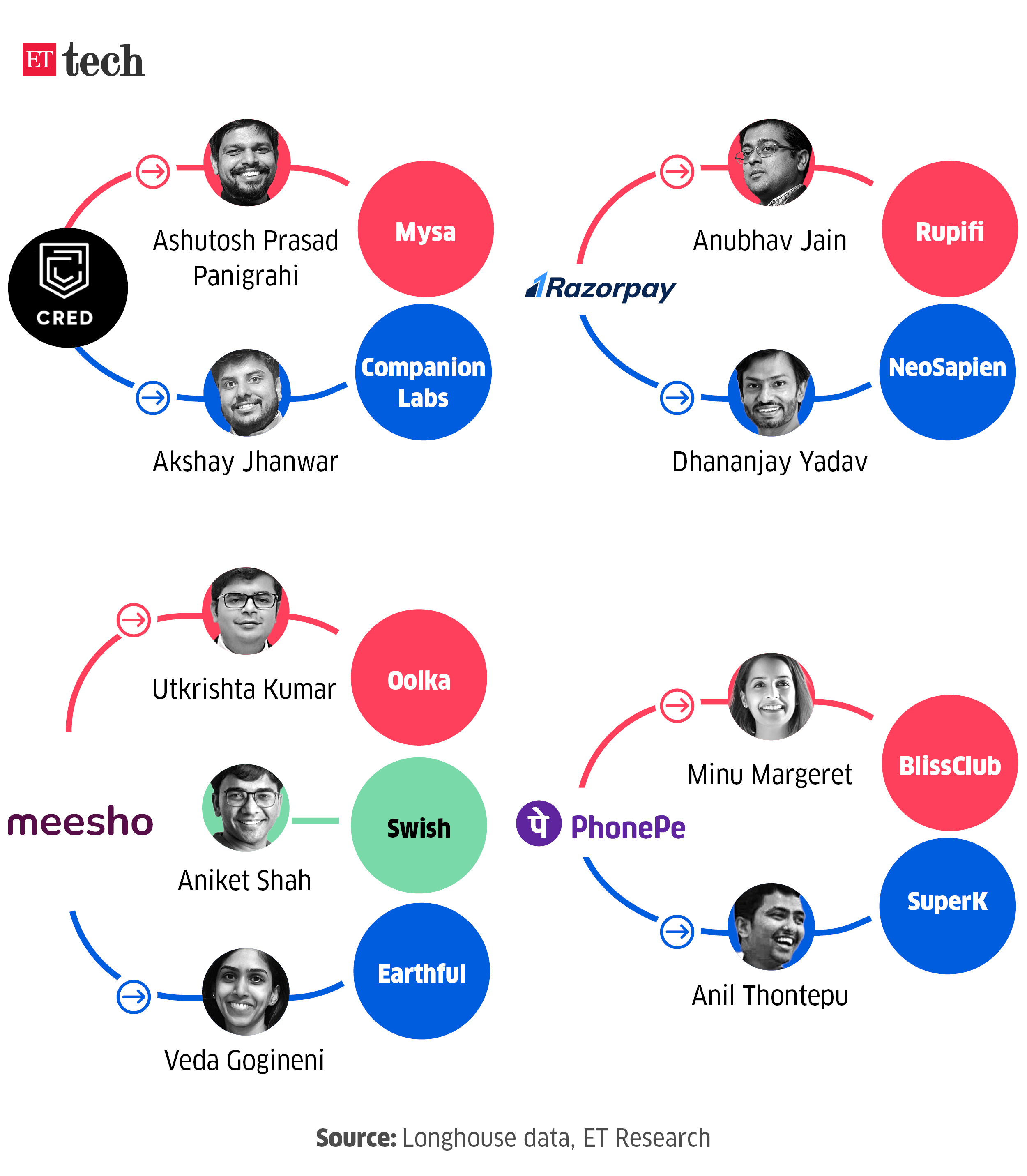

In this generation, payments firm Razorpay leads the pack, having produced 39 founders, closely followed by fintech Cred with 38. Value commerce platform Meesho has hatched 27 entrepreneurs, while digital payments major PhonePe has birthed 22.

“Startup Mafia 3.0 reflects a more mature and expansive entrepreneurial ecosystem, compared with earlier waves,” said Anshuman Das, chief executive and founder, Longhouse.

ETtech

ETtech

Wider backing

“The investor landscape has also expanded significantly, with a wide range of funding sources including angel investors, family offices, early-stage venture capital firms and specialised thematic funds,” Das said, adding that founders no longer need to rely solely on large global investors; smaller and more specialised funds are willing to back niche ideas.

While the trend has long existed, executives are now confident of building in new domains. Many are building in niche segments such as AI-native products, cross-border payments, gaming and services tailored for India’s tier II markets.

The current generation includes a broader mix of founders, both younger professionals and seasoned operators with 15-20 years of experience.

ETtech

ETtech

Investors said employees from hyper-growth startups understand early on how to build and scale companies. “When you have been on the inside of a company growing fast, you don’t need to learn the basics; you already know what great looks like,” said Rahul Taneja, partner at Lightspeed Venture.

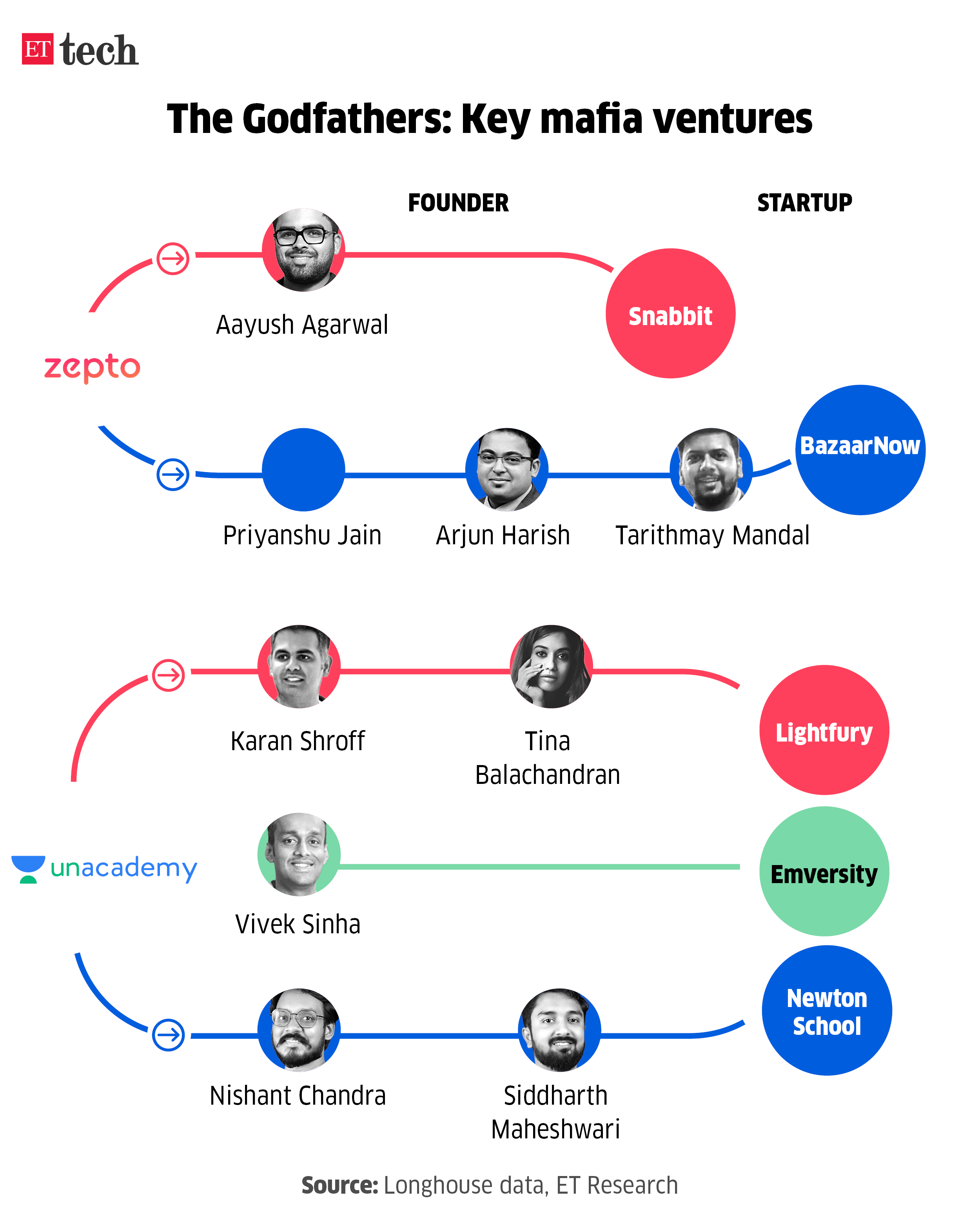

Lightspeed, which recently raised $9 billion in fresh capital, has backed several such founders emerging from startup ecosystems, including Aayush Agarwal, previously at Zepto, who went on to build Snabbit; and Utkrishta Kumar, earlier Meesho’s chief business officer, who is now building Oolka, an AI-powered credit management app.

Other major ‘mafia’ startup founders include former Udaan CFO Rishi Kedia and cofounder Amod Malviya, who together launched Pre6, which helps streamline manufacturing operations.

Minu Margeret, former brand manager of PhonePe, founded Blissclub, a D2C activewear brand.

Reduced gestation

The gap between working at a startup and launching a company has shrunk sharply for this generation of founders. Razorpay, founded in 2014, alone has birthed one founder every year since 2017.

“Now we are seeing startup founders emerging from younger companies like Zepto too. It is not a small change but a dramatic leap for the ecosystem,” said Dipanjan Basu, cofounder and partner, Fireside Ventures.

Founded in 2021, Zepto has already spawned Snabbit, valued at $180 million, and early-stage companies such as Loop, RNTL, BazaarNow, and Capinity Partners thanks to reduced gestation periods, Longhouse data showed.

According to Anant Vidur Puri, partner at Bessemer Venture Partners, the pace at which startup executives gain experience has dramatically increased. “The way we think about this cohort of founders is deliberate. We’re not simply pattern-matching on pedigree — we’re evaluating what someone has already navigated,” he said.

Mafia matters

Vineet Khanna, cofounder of Supertails and former executive at Licious, said the experience of scaling a company rapidly prepared him for entrepreneurship. “Preparedness for scale was the biggest learning.”

“When I joined along with Varun (the other cofounder of Supertails), Licious was just a two-city company, maybe even a tad below a Rs 1 crore per month kind of revenue, with aspirations to grow manifold. What followed in the next three years was a lot of scaling,” he added.

Investors say such founders bring operational maturity to the table. “They also have deep personal networks, which means they can build high-quality teams much faster,” said Taneja of Lightspeed.

Take Oolka’s Kumar, for instance. Besides opening doors when he was raising funds, his five-and-a-half years at Meesho also helped rope in talent. “A lot of Meesho ex-employees joined us, some even took pay cuts because they believed in our journey at Oolka and our ability to execute.”

Why the risk?

A deeper VC pool, easier access to AI tools and rising consumer spending are encouraging more to take the entrepreneurial leap. Government support through schemes and policy initiatives also plays a positive role, pushing individuals to take the risk. A growing number of Esops (employee stock ownership plans) and liquidity events have also helped.

“Now, employees are seeing more liquidity events, Esop payouts, and secondary sales as startups succeed. That has motivated many professionals to view startups as a viable career path,” said Tina Balachandran, cofounder, LightFury Games, a AAA game-tech company dedicated to creating immersive experiences. “Earlier, people were hesitant because they were concerned about their (career) stability, but that perception has changed significantly.”

Balachandran was with the edtech startup Unacademy before starting LightFury with Karan Shroff, after the edtech industry suffered in the post-Covid years. “Edtech businesses had to rethink cost structures, which led many of us to reflect on our careers,” she said.

The company raised $8.5 million in a round led by Blume Ventures. She added that nearly 95% of LightFury’s employees hold ESOPs so that “every person in the organisation has skin in the game.”

A report by Orios Venture Partners found India was the world’s most active IPO market in 2025, which saw 20 VC-backed startups listing on the bourses. These included consumer and digital-first companies such as Groww, Physics Wallah, Meesho, and Urban Company.

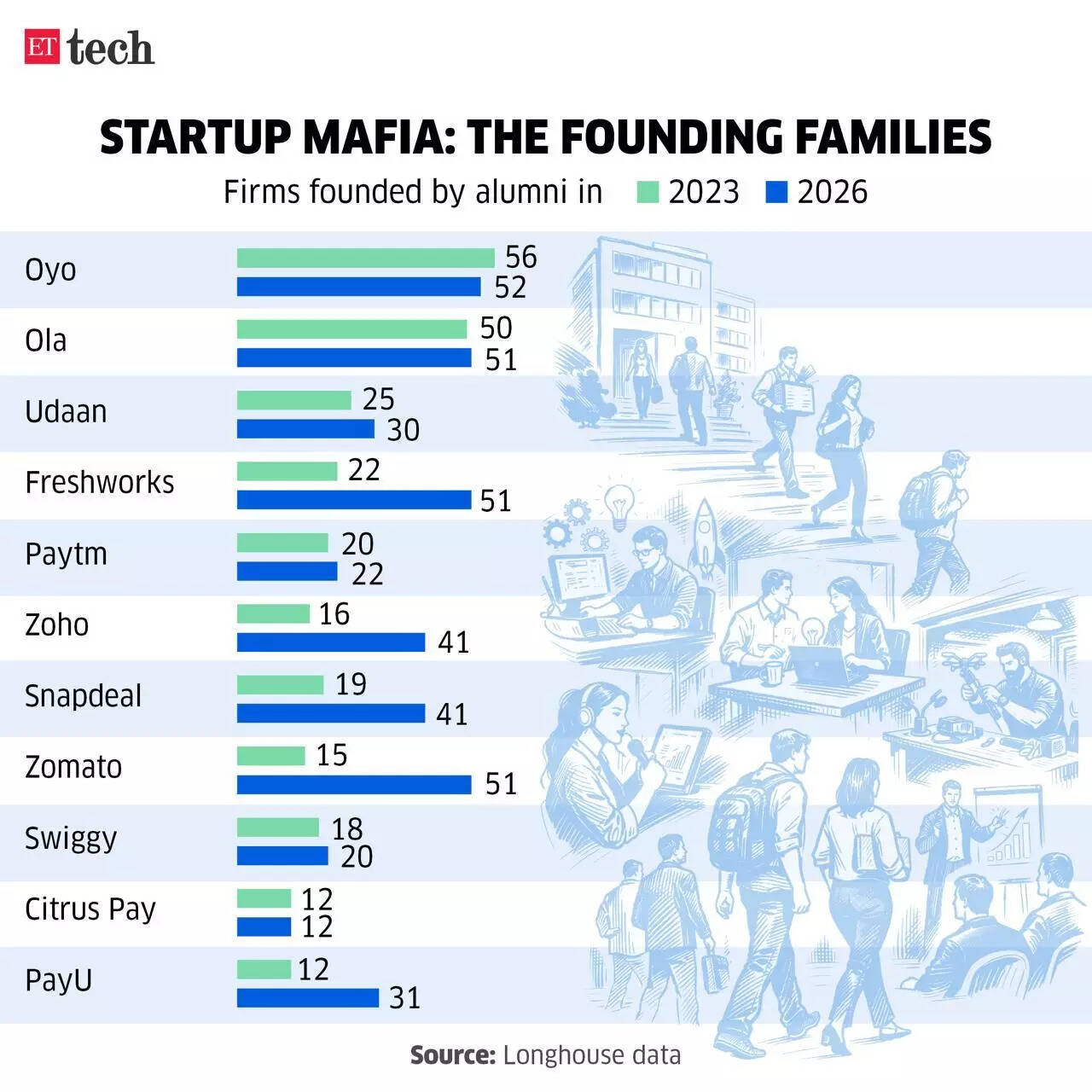

In 2023, ET reported that the first generation of startups gave rise to 253 startups in the second cohort led by firms such as Zomato, Freshworks, Paytm and Citrus Pay. This number has jumped to 360 as of March 2026, according to Longhouse data.