When this inflationary mindset takes off, inflation becomes like a runaway train.

By Wolf Richter for WOLF STREET.

The problem is that even before fuel prices began to spike, inflation had already been accelerating and running hot, and the current fuel price spikes will add to it, just when the economy has become more forgiving of price increases. That’s very bad timing:

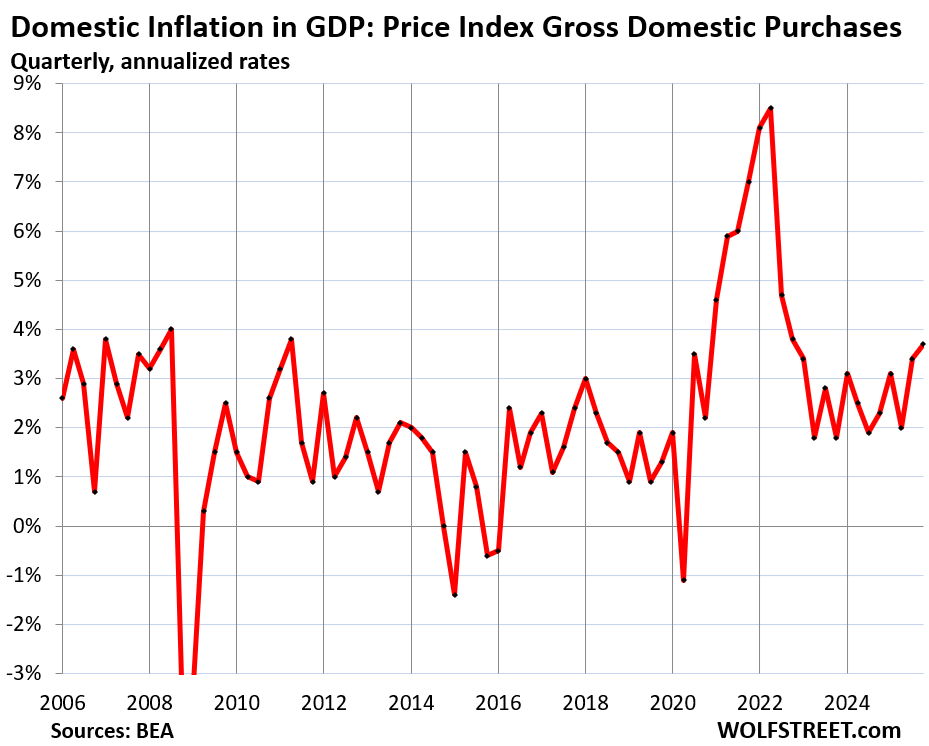

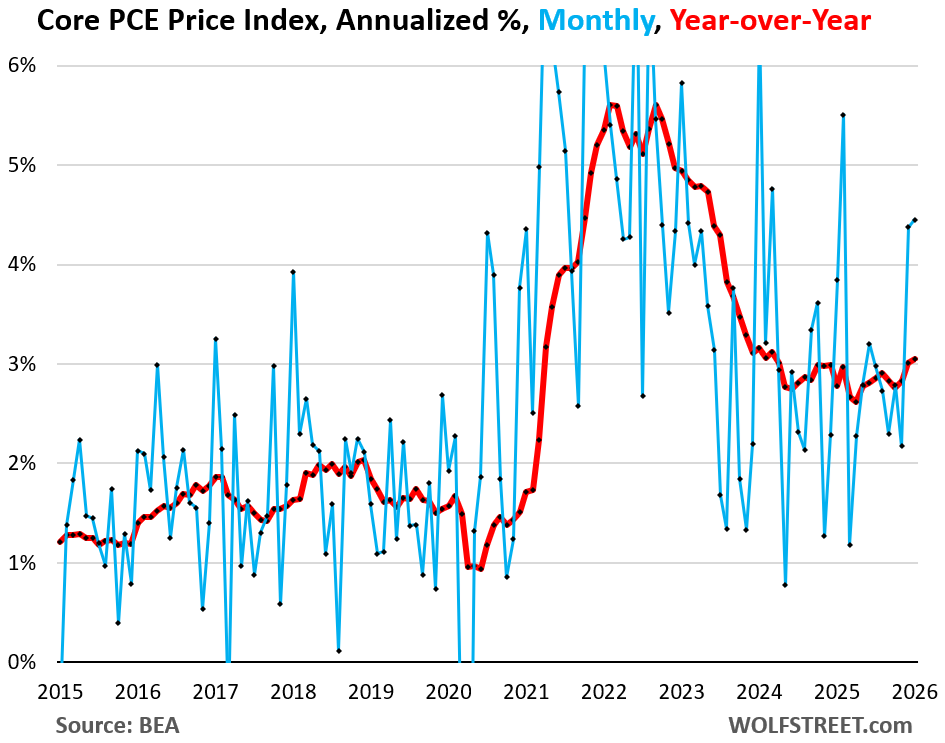

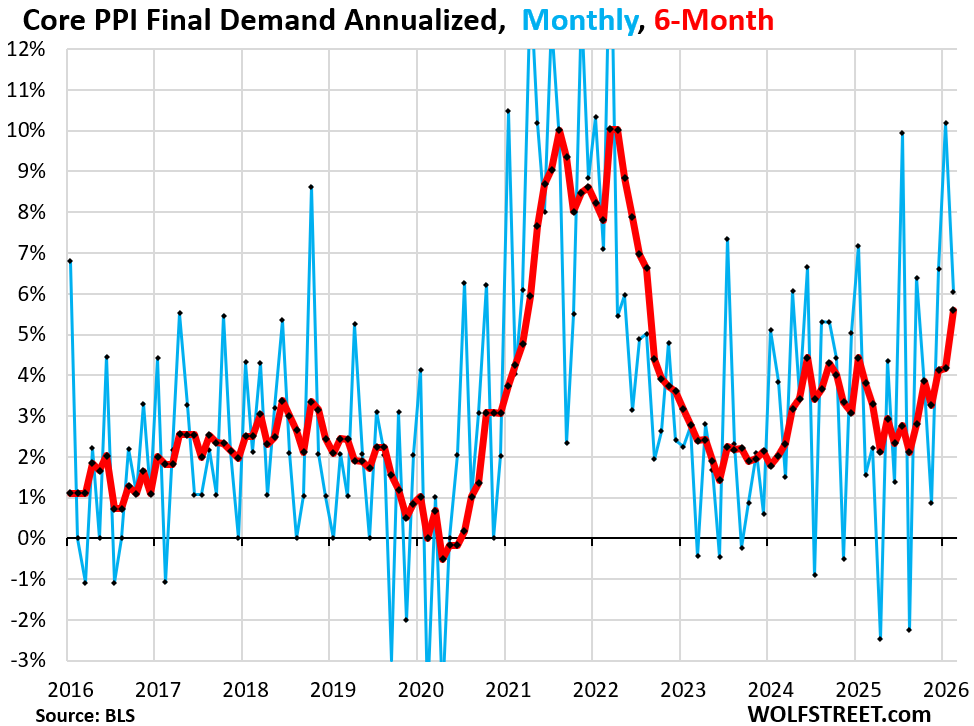

The broadest inflation gauge, which tracks inflation across GDP and not just consumer-facing inflation, rose by 3.7% in Q4. The price index in GDP that excludes imports rose by 3.8% in Q4, the worst since 2022. The core PCE Price Index, the Fed-preferred inflation index for consumer price inflation, rose by 3.1% in January, the worst in nearly two years. The core Producer Price Index, which tracks inflation that companies face, jumped by 5.6%, the worst since August 2022 (see charts at the bottom of the article).

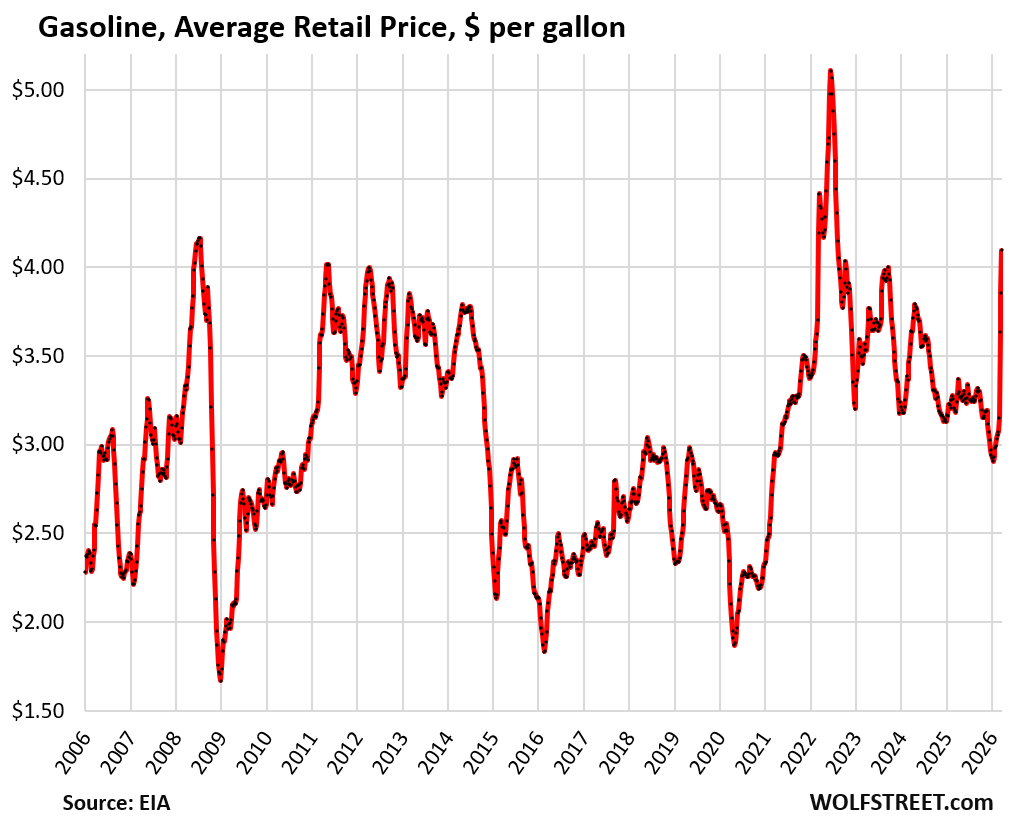

The average retail price of gasoline, all grades combined, at gas stations on Monday spiked by another $0.24 from the prior week, and by $1.17 or by 40% since the beginning of the year, to $4.10 per gallon, the highest since August 2022, according to EIA data released this morning, based on a survey of gas stations on Monday.

These price increases of gasoline will enter into the inflation calculations for the Consumer Price Index (CPI) and the Fed-preferred PCE price index for March, to be released in April; and they will push up the broad GDP inflation measures for Q1.

The three-and-a-half-year long decline in gasoline prices from over $5 in mid-2022 to $2.91 in early January was a substantial contributor to the cooling of overall consumer price inflation rates. And that impetus has done a U-turn. Overall inflation measures for March will show that U-turn, and will be hot.

But gasoline price spikes unwind: In early January 2026, gasoline cost the same as during some periods in 2007 and 2008, and a lot less than during part of the time in between.

When gasoline prices fall back to earth, they push down inflation, which is why the Fed could be tempted to “look through” (meaning, ignore) the spike of gasoline prices.

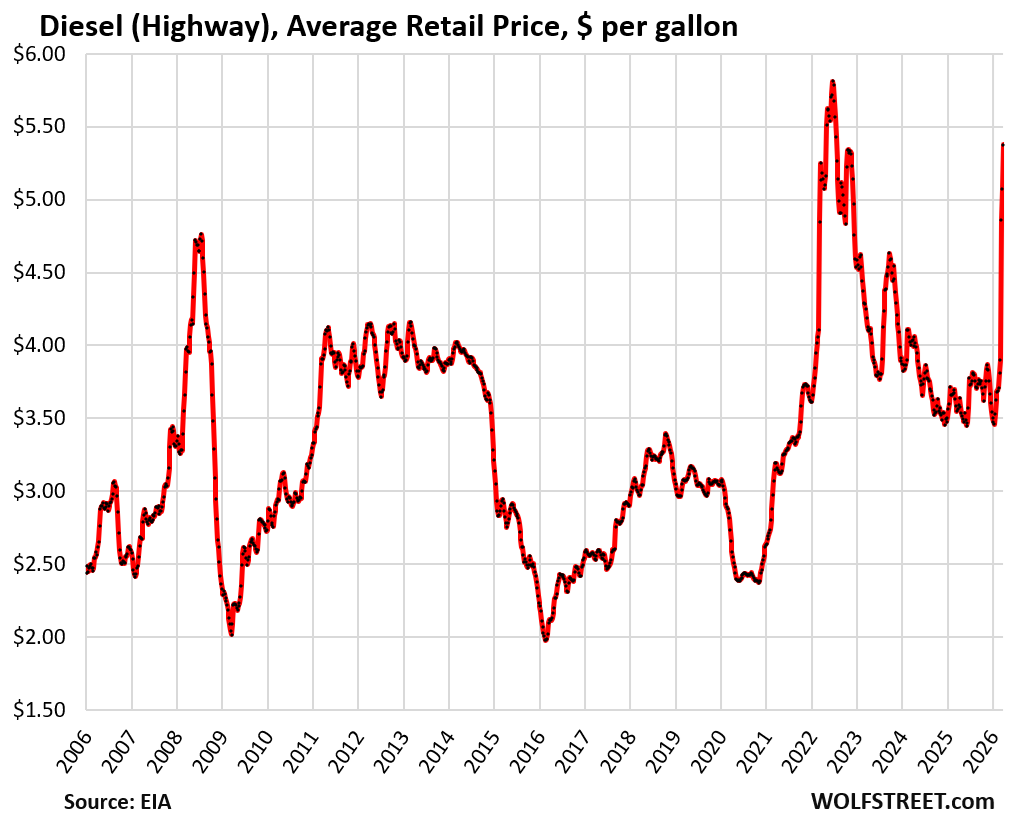

But diesel is a serious problem for core inflation. The price of highway diesel on Monday spiked by another $0.30 from the prior week, and by $1.90 or 55% from the beginning of the year, to $5.37 per gallon. Year-over-year, the price of diesel jumped by 51%!

Only a small portion of consumers drive vehicles with diesel engines – some pickups and SUVs, and some older European imports.

But diesel prices feed into transportation costs, and they feed into costs of goods and transportation services that companies pay for, and they will try to pass those costs on via higher prices of goods and services that eventually filter through to the end-users, including consumers. And those prices of goods and services are part of core inflation measures.

The daily spot price of jet fuel has doubled since early January. Airlines are aggressively trying to pass those cost increases – a substantial part of their overall costs – on to their ticket prices, and if people continue flying, rather than forgoing trips that are suddenly a lot more expensive, those price increases could stick.

Many airlines hedge part of their fuel purchases, so their cost increases don’t exactly track the spike of the spot price of jet fuel.

Airline fares are part of services inflation and are part of the core inflation measures. Thankfully for consumers, airlines have a history of being forced to eat higher fuel prices and book losses as they could not raise fares without losing a lot of business. But they’re trying.

Air freight also faces higher fuel costs, and that impacts all kinds of transportation costs that could filter into prices of goods and services.

Ocean shipping and transportation by rail also face higher fuel prices. And carriers will also try to pass on those costs, and all this is additive.

Fuel price spikes could trigger the inflationary mindset, when consumers are willing to pay those higher prices, and demand higher wages, and companies are willing to pay those higher wages to their workers and higher prices for goods and services they need, knowing that they can pass on those costs plus some to the next entity, and ultimately plus-some to consumers, which is what happened in 2021 and 2022, amid a historic spike in profits, and in the 1970s. When this inflationary mindset takes off, inflation becomes like a runaway train.

The Fed can deal with this by hiking its short-term policy rates to whack the inflationary mindset out of the minds of businesses and consumers. It doesn’t always work and it can get messy, but that’s the main tool the Fed has when the inflationary mindset takes off. Alternatively, it could try to prevent the inflationary mindset from even taking off by responding quickly with rate hikes – something it failed to do when that inflationary mindset began taking off at the end of 2020, and the Fed didn’t initiate the first feeble rate hike until March 2022.

Current inflation gauges, which still predate Iran war, were already hot:

Inflation as tracked across the economy in GDP, except imports, in Q4: +3.8% annual rate.

Core inflation that consumers face, which excludes energy and food, as tracked by the Fed-favored Core PCE price index: +3.1% year-over-year (red), worst in nearly two years. The Fed’s target for this measure is 2.0%.

Core inflation that businesses face, as tracked by the Core PPI Final Demand: +5.6% six-month average annualized (red), the worst since August 2022.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()