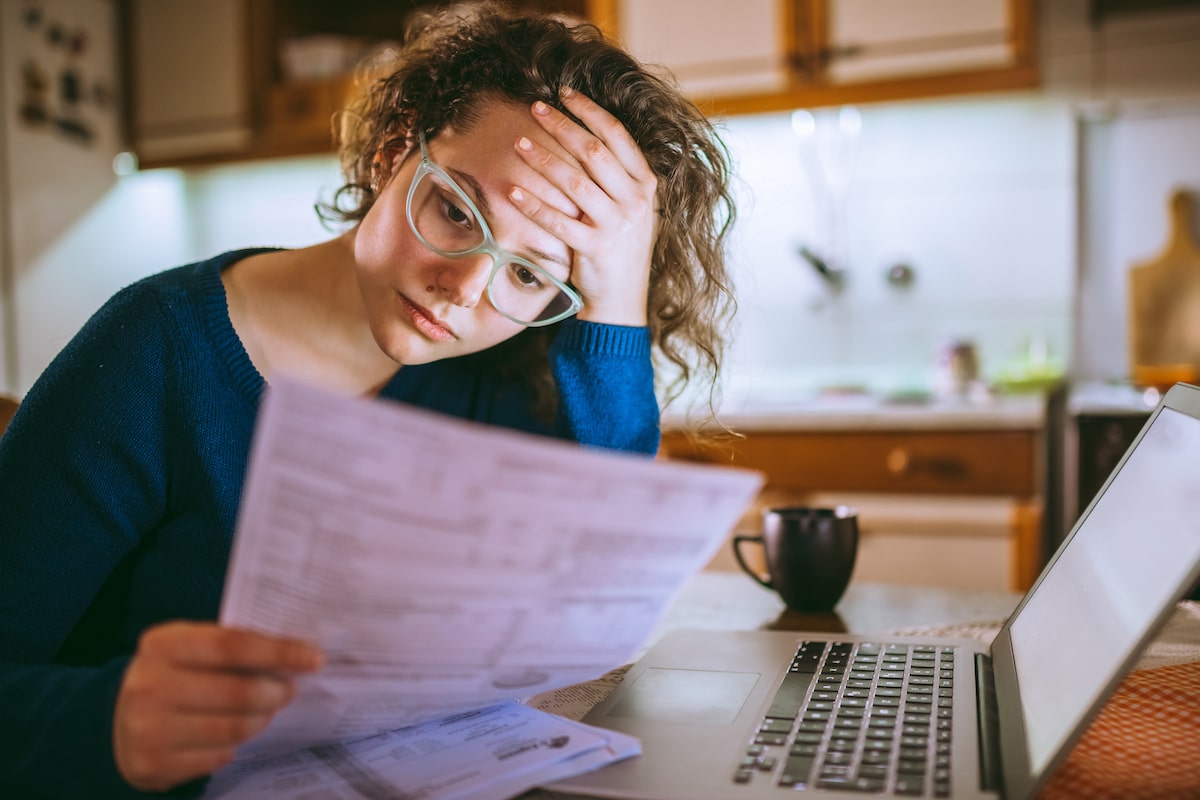

A recent survey found that money is a top stressor for many Canadians, outweighing work, health and relationship stress.GETTY IMAGES

While working as a personal financial planner at a major Canadian bank, Aseel El-Baba came up with the radical notion to redesign her traditional office space to feel like a therapist’s office. Ms. El-Baba replaced rolling chairs, overhead lighting and charts and graphs with candles, a vision board and even blankets.

The redesign wasn’t about décor – she wanted clients to feel safe.

“Money is already a sensitive and hard topic,” says Ms. El-Baba, who left traditional financial planning in 2020 to study psychotherapy. Now, she is a member of the Financial Therapy Association and runs Holistic Optimal Wealth, a Toronto-based financial therapy practice that helps clients navigate the emotions and stressors of money.

Her pivot reflected a pattern she was seeing with clients: People struggle not just with finances, but with the emotions behind them.

Rising pressures

For many Canadians, financial worries outweigh work, health and relationship stress. FP Canada’s 2025 Financial Stress Index found that 42 per cent of survey respondents named money as a top stressor, with nearly half losing sleep over it. Everyday costs drive much of the stress: over two-thirds cited grocery prices while 54 per cent blamed inflation.

Halifax-based money coach April Stroink says people often carry financial stress because they adopt money as part of their identity. “Then add social media – it’s like ‘keeping up with the Joneses’ on steroids,” she says.

For many Canadians, these stressors compound. The Financial Stress Index found more than half of Canadians say financial stress affects their lives, with 38 per cent reporting anxiety, depression or other mental-health impacts. Nearly one in five say it causes reduced productivity or relationship strain, with others noting family conflict or substance use.

While these findings are alarming, experts say there are practical steps Canadians can take to reduce financial stress and regain a sense of control.

Recognize patterns

Ms. Stroink says when she starts working with a client, she asks about their early experiences with money.

“That can tell a lot about somebody [and] what their money decisions are as adults,” she says. Those first experiences often set the patterns that affect you later in life, she adds. For example, someone whose parents avoided talking about money may follow a similar pattern and ignore their bank book.

Patterns around money can emerge in many ways, from impulse buying and avoiding bills to feeling guilty about debt or letting social pressure influence the way you spend. Ms. Stroink says it’s critical to be honest with yourself and acknowledge those behaviours before you can build a plan to change those habits.

Avoid triggers

Jessica Moorhouse, certified financial counsellor and author of Everything but Money: The Hidden Barriers Between You and Financial Freedom, agrees that unhealthy financial habits can stem from the way your parents approached or spoke about money in your childhood. But awareness only goes so far, she says. Recognizing current-day triggers is key to reducing financial stress.

“You need to identify what those feelings are and what triggered them,” she says. “Usually it is a specific event or instance – something you saw online, something you heard.”

Feeling inadequate compared to your peers globetrotting lifestyle? Worrying you’re missing out on a trendy get-rich-quick investment scheme? Scrolling social media for hours in the evening can add anxiety, says Ms. Moorhouse, so capping your Facebook, TikTok or Instagram time may be a good idea to keep those feelings of stress in check.

Because money stress often comes from uncertainty, a financial inventory can help you feel better about your situation.GETTY IMAGES

Ground yourself

Ms. Moorhouse says it can be helpful to do a financial inventory to see where you are, money-wise. Check how much you have saved up in case of unexpected costs like car or home repairs, vet bills or a job loss. Money stress often comes from uncertainty, she says, so “it can be a nice reminder that it’s not as bad as it may seem.”

That inventory can also help you identify where to focus your efforts with practical strategies.

“An emergency fund works, paying yourself first works, keeping your debt low and eliminating that as soon as possible works,” Ms. Moorhouse says. “You know what’s really great about having cash in the bank? It makes you feel safe.”

Regulate emotions

Ms. El-Baba says stress can hijack your nervous system, making even simple financial decisions feel overwhelming. She emphasizes the importance of regulating your body first. “A big part of financial literacy is actually emotional literacy – your ability to identify emotions, to feel them and release them in a safe way,” she says.

Simple practices like deep breathing or somatic grounding – focusing on the physical sensations of the body while in an emotionally charged state about finances – can restore a sense of safety. It gives you the bandwidth to approach budgeting, debt and saving with clarity instead of panic, says Ms. El-Baba.

Break the cycle

Ms. Stroink says a simple but powerful tool is to take a 24-hour pause before making a significant financial decision. It gives you space to reflect, regulate your emotions and make choices from a calmer, more rational place.

In her view, progress comes from pairing self-awareness with a financial plan or saving and spending system that’s easy to follow and simplifies your finances enough to keep you from sliding back into old patterns.

“If something stresses you in your life, you’ll revert back to those habits where you feel most comfortable,” she says. “So you really need a solid system that will support you in that time.”